When inflation is above that target, the Bank can decide to put rates up. This encourages people to spend less, reducing demand for goods and services and limiting price rises.

Once inflation is at or near the target, the Bank may hold rates, or cut them to stimulate spending and economic growth.

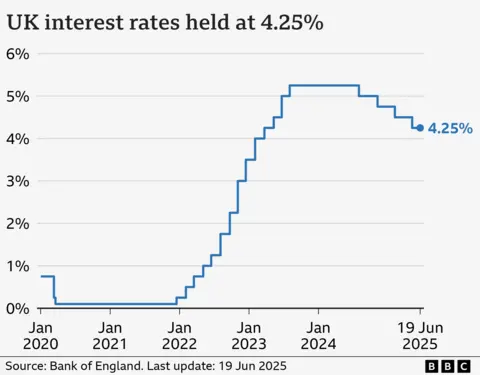

What has happened to UK interest rates?

The Bank of England cut rates in August and November 2024, and again in February and May 2025, taking rates to 4.25%.

Although it held rates at that level in June, the Bank of England governor Andrew Bailey indicated that further “gradual and careful” cuts could follow, perhaps as early as the summer.

Will rates fall further?

It is difficult to predict exactly what will happen to interest rates, even in the medium-term.

About 600,000 homeowners have a mortgage that “tracks” the Bank of England’s rate.

But the vast majority of mortgage customers have fixed-rate deals. While their monthly payments aren’t immediately affected by a rate change, future deals are.

Mortgage rates are still much higher than they have been for much of the past decade.

As at 16 July, the average two-year fixed mortgage rate was 5.03%, according to financial information company Moneyfacts, and a five-year deal was 5.01%. The average two-year tracker was 4.91%.

This means many homebuyers and those remortgaging are having to pay a lot more than if they had borrowed the same amount a few years ago.

About 800,000 fixed-rate mortgages with an interest rate of 3% or below are expected to expire every year, on average, until the end of 2027. Their borrowing costs are expected to rise sharply.

You can see how your mortgage may be affected by future interest rate changes by using our calculator:

Credit cards and loans

Bank of England interest rates also influence the amount charged on credit cards, bank loans and car loans.

Lenders can decide to reduce their own interest rates if Bank cuts make borrowing costs cheaper.

However, this tends to happen very slowly.

Getty Images

Savings

The Bank base rate also affects how much savers earn on their money.

A falling base rate is likely to mean a reduction in the returns offered to savers by banks and building societies.

The current average rate for an easy access savings account is 2.67%, according to Moneyfacts.

Any cut in rates could particularly affect those who rely on the interest from their savings to top up their income.

What is happening to interest rates in other countries?

In recent years, the UK has had one of the highest interest rates in the G7 – the group representing the world’s seven largest so-called “advanced” economies.

In June 2024, the European Central Bank (ECB) started to cut its main interest rate for the eurozone from an all-time high of 4%.

In the US, the central bank – the Federal Reserve – cut rates three times in the latter part of 2024.

However the Fed has since held interest rates – most recently on 30 July. This means the bank’s key lending rate’s target range remains at 4.25% to 4.5%.

The system will be officially unveiled by Minister of Home Affairs, Leon Schreiber at the Tourism Business Council of South Africa’s annual conference.

According to the government, the platform will initially process tourist visa applications for short stays of up to 90 days.

By the end of September, the system will go live at Johannesburg’s OR Tambo International Airport and Cape Town International Airport, before gradually expanding to other ports of entry and additional visa categories.

Minister Schreiber has described the initiative as a critical step toward eliminating inefficiencies and fraud: “Over time, the ETA will be expanded to more visa categories and rolled out at more ports of entry. This scale-up will continue until no person can enter South Africa without obtaining a digital visa through the ETA.”

A shift from paper to digital

The ETA builds on promises made by President Cyril Ramaphosa during his February State of the Nation Address, where he pledged to digitize immigration processes.

However, questions remain about the future of South Africa’s existing e-Visa portal, which currently serves over 30 countries.

Authorities have yet to confirm whether the ETA will replace or operate alongside the e-Visa system, raising concerns over possible duplication for travelers.

Africa’s need for openness

While the ETA aims to strengthen security and streamline border processes, experts say South Africa’s move also highlights a broader challenge: African countries remain less open to each other than to the rest of the world.

Intra-African visa restrictions have long been cited as a barrier to deeper trade and tourism links.

Greater openness, facilitated by modern systems like ETA, could help African nations unlock the full potential of the African Continental Free Trade Area (AfCFTA).

Easier cross-border movement would not only boost tourism but also support small businesses, regional logistics, and labor mobility, which are all essential for building competitive economies on the continent.

The bigger picture

South Africa’s ETA may be a milestone for its tourism and border security, but its broader significance lies in setting a regional precedent.

As African countries digitize entry systems, the real opportunity lies in aligning these policies to make cross-border travel smoother for African citizens.

If deployed strategically, ETA systems could help turn Africa’s longstanding vision of free movement, and by extension stronger intra-African trade, into a practical reality.

The acquisition will enable the organisation to extend its AI capabilities.

US-based Enterprise software company Workday has announced plans to acquire AI platform Sana, in a deal valued at $1.1bn. By acquiring Sana, Workday aims to leverage the company’s AI knowledge and further itself amid a landscape that is focused on AI innovation.

“Sana’s team, AI-native approach and beautiful design perfectly align with our vision to reimagine the future of work,” said Gerrit Kazmaier, the president for product and technology at Workday.

He added, “This will make Workday the new front door for work, delivering a proactive, personalised, and intelligent experience that unlocks unmatched AI capabilities for the workplace.”

Under the terms of the definitive agreement, Workday will acquire all of the outstanding shares of Sana for approximately $1.1 bn. The deal is expected to close in the fourth quarter of the fiscal year in 2026.

The acquisition comes amid a time in which organisations across the globe are racing to implement AI technologies to address and even assume the challenges that arise in the workplace.

For example, in the past few months alone French technology services company Capgemini acquired US-based WNS to extend its AI reach. Aryza, a Dublin-based SaaS provider acquired conversational artificial intelligence provider Webio for an undisclosed sum and OpenAI said it was buying Io, an AI start-up founded by former Apple design chief Jony Ive and several former Apple engineers.

Several governments too have unveiled broad spectrum plans to incorporate artificial intelligence into their national strategies, with a focus on business growth and improving the lives of citizens.

But significant concerns have been raised about AI’s potential to replace humans in the workforce, as agentic AI tech is further developed and topics of ‘onboarding AI’ become more mainstream.

Forrester vp and principal analyst Craig Le Clair recently discussed the issue of ‘AI employees’, explaining that AI-led layoffs are not far off and that he would expect job descriptions for an AI agent to be a reality by 2027.

Don’t miss out on the knowledge you need to succeed. Sign up for the Daily Brief, Silicon Republic’s digest of need-to-know sci-tech news.