Here at FT Alphaville we love exploring “black hole” companies: those ultra-private businesses that must largely be observed by the influence they exert on others.

But even within that category, there aren’t many places quite like Valve Corporation, with its bizarre corporate structure, revenue-per-head figures that would make Silicon Valley or Wall Street giants hot and bothered, a product that seems to basically print money, and a seldom-seen leader deified in some corners of the internet — all without ever taking outside investment.

Few companies can claim a bigger role in video game history than Valve. Founded in 1996 by Gabe Newell and Mike Harrington — both former Windows developers at Microsoft — the company’s first title, Half-Life, launched in 1998, is widely credited with transforming the first-person shooter genre. Harrington left the company in 2006, leaving Newell (known to some online obsessives as “Gaben”) as its de facto head.

Valve games have been few in number, but their influence is huge: Half-Life and its sequels for their storytelling; Portal for its creativity and humour; the Counter-Strike series for its role in the emergence of esports; Left 4 Dead for its use of artificial intelligence to create dynamic co-operative gameplay. However, its most influential title is arguably Team Fortress 2, the game whose cosmetics system brought microtransactions — where players pay small amounts to unlock in-game content — into the mainstream.

In doing so, it created a business model that has, for better and for worse, powered the mobile games revolution of the past two decades — and laid the groundworks for one of the zanier presentation slides we’ve seen outside of SoftBank:

Valve has even managed to find some success in the notoriously tricky hardware market. Its handheld console — which looks roughly like a military-grade Nintendo Switch — has sold “multiple millions”, the company claimed in late 2023, with market research firm IDC estimating it hit 6mn sales by early this year.

But its financial engine, powering almost all its other achievements, is Steam. For a generation of gamers, Steam needs no introduction — such is its dominance. But for those blissfully unaware, Steam is a storefront, distribution service and social media network for PC gamers that launched in 2003.

And it basically prints money.

Personal computers have been a tricky proposal for game developers. In the early ’00s, pirating PC games was pretty straightforward. Most titles sold as a physical disc with a unique serial code, but these could easily be faked.

For developers, this was obviously anathema. Digital rights management — controlling who could use game software — became an increasingly urgent topic.

In came Valve. After unsuccessfully pitching to companies including Microsoft, it developed Steam, which combined game-updating technology, anti-piracy and anti-cheating measures on one platform. It would sell users games and verify that they owned the game — virtually eliminating the need for discs and serial codes.

Steam landed in the right place at the right time, quickly becoming the default platform for PC gamers to download and manage their games. Safer and more convenient than piracy, it also introduced a social overlay that allowed players to communicate more easily while playing different games.

“The real value proposition for something like Steam is to have everything in one place,” says Clay Griffin, an analyst at MoffettNathanson. “It’s a one-stop shop.”

As a result, Steam has established a dominant position in the PC games industry, with analysts assuming it accounts for perhaps 70 per cent of all sales of such games. That equates to a significant chunk of what market research firm Newzoo reckons is a $40bn sector (including hardware). The platform has more than 100,000 titles available for download, dwarfing its competitors, and levies a typical 30 per cent commission on sales of games and their (often extensive) add-ons.

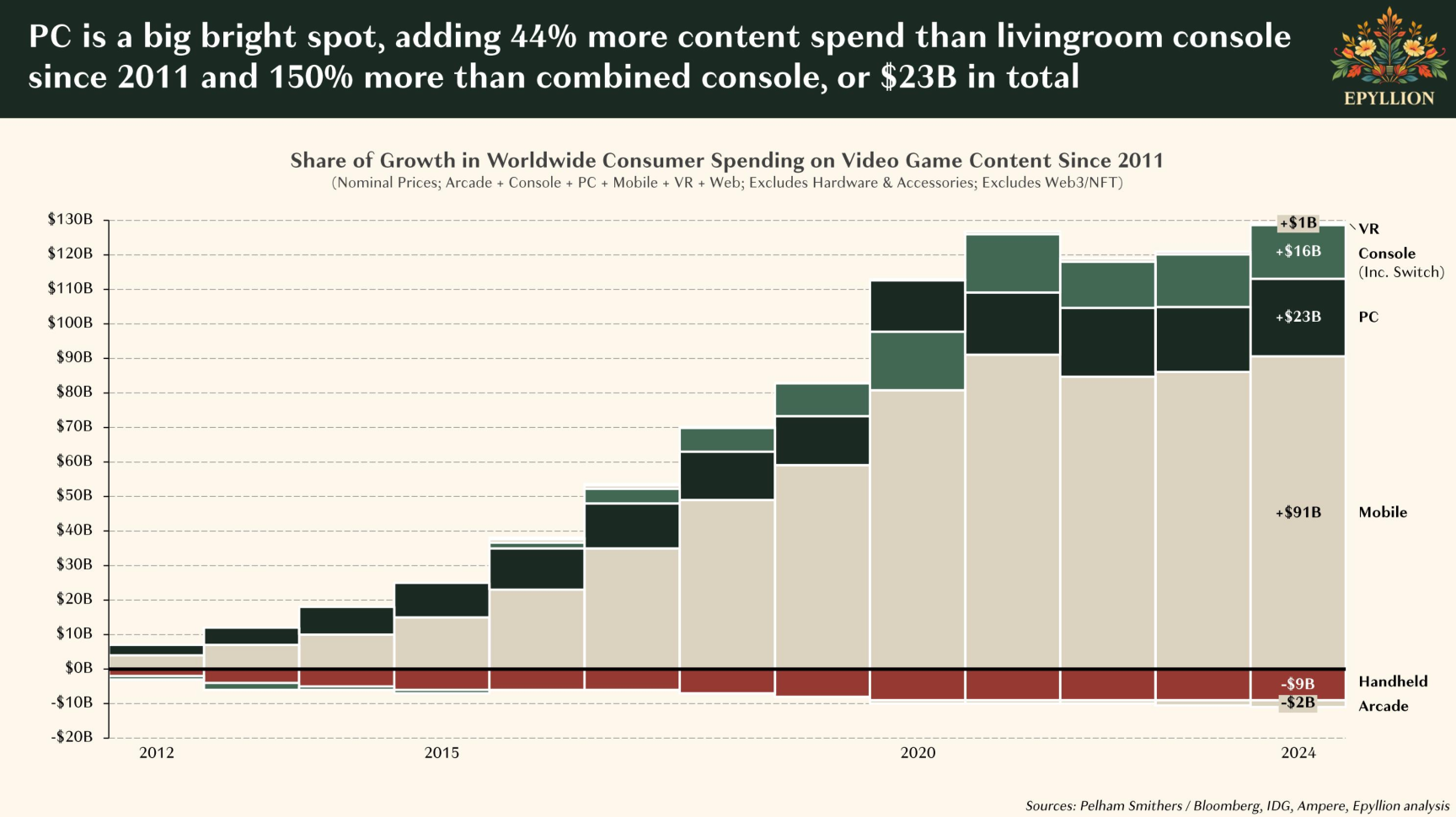

And it’s good to be the king. Amid a sustained period of stagnation for consoles, spending on PC games has seen healthy increases. In a presentation shared earlier this year, Matthew Ball, at investment adviser Epyllion, identified PC as a “big bright spot” amid a difficult patch for traditional gaming vectors (high res):

Steam’s concurrent player figures hit a record high earlier this year following double-digit annual growth, prompting Goodbody analyst Patrick O’Donnell to tell clients that Steam “now owns the PC distribution channel” — if it didn’t already — with “significant advantages” in engagement against its rivals. Based on Steam users’ language choices, much of the growth comes from China.

Advisory firm Ampere Analysis estimates that Steam had 170mn global active monthly users in May, up from 153mn the year before. Remarkably, average concurrent users are about three times the number who are actually playing games.

Piers Harding-Rolls, Ampere’s games research director, said this “highlights that many users automatically sign into the platform and also that Steam represents more than a PC game storefront — it’s a gaming community platform in its own right with millions visiting the app to engage with other users”.

If generative AI does — as some optimists hope — remove development barriers to create a supply-side revolution in gaming content production, Valve may find itself selling shovels in a gold rush.

Working out how much money Valve already makes from its dominance of PC gaming is tricky. Newell is presumed to be its biggest shareholder, and the company is intensely private. It makes almost no financial disclosures, and its employees seldom give interviews to the press.

Still, there are some clues.

In 2021, developer Wolfire Games sued Valve, alleging it was distorting the PC games market by imposing “platform most-favoured nation” clauses on sellers — forcing them to offer their best price on Steam.

Other individual customers launched a lawsuit against Valve over pricing last summer, and a judge ruled last year that their case could be brought together with Wolfire’s in a class-action suit — opening the door to other developers joining in. Their allegations are broad, but focus on the notion that without Steam’s dominance, average commission rates across the sector would be lower: improving developers’ margins and/or lowering consumer prices.

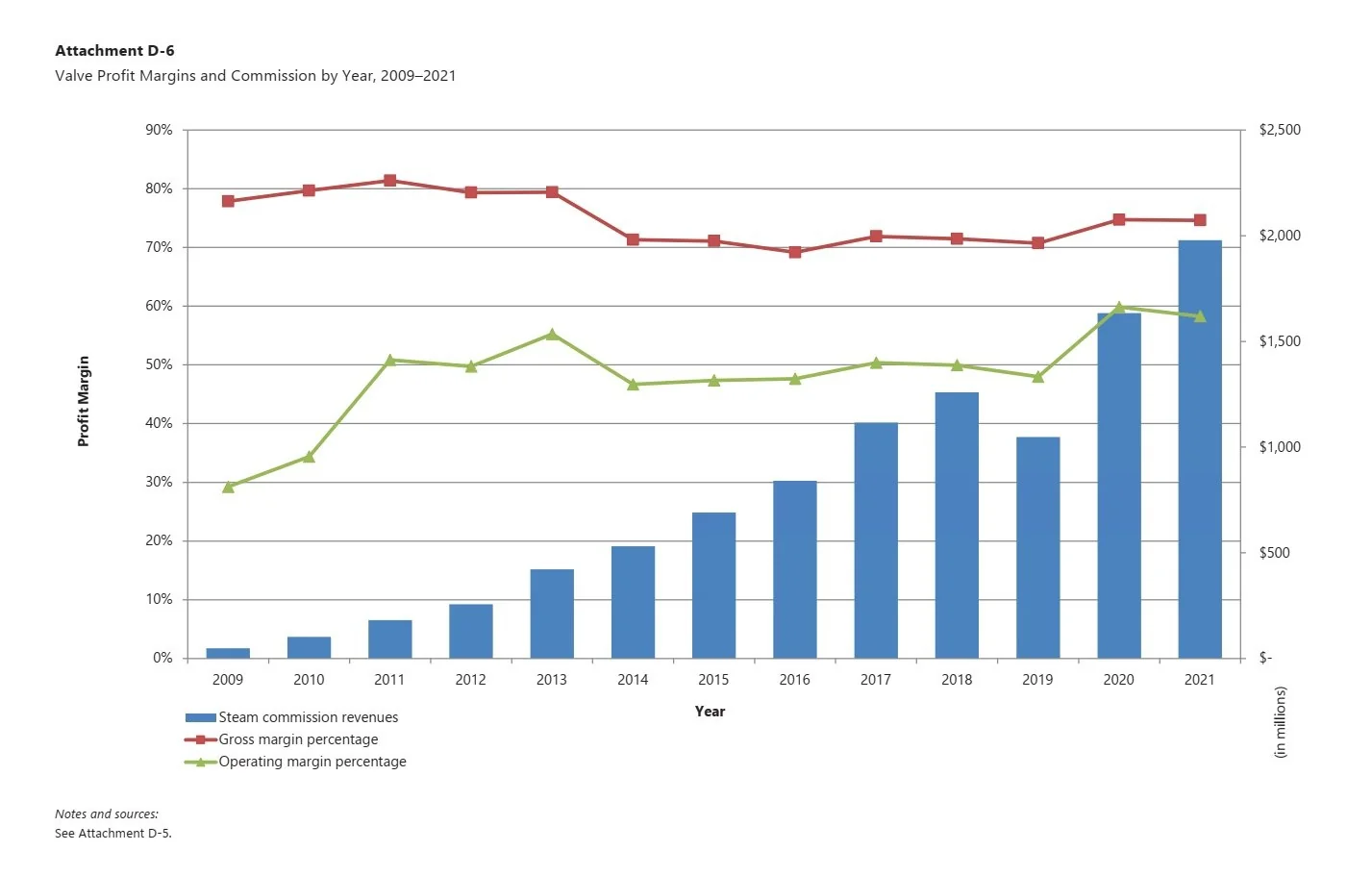

Improperly redacted documents from the initial Wolfire case — later hidden — indicated that Valve had only 336 staff in 2021, with just 79 of them working on Steam. We’ve remade it using data reported contemporaneously:

The public docket also briefly contained another chart, which purported to show Steam’s commission revenues and, uh, healthy margins (high res here):

We’re all mature, grown-up blog writers/readers here, so let’s have a discussion about sources and numbers.

This is a screenshot of a document we can no longer access. Pavel Djundik, creator of SteamDB, a Steam data platform, is cited by contemporaneous reports as having spotted the data underpinning the staff headcount chart above. Djundik subsequently tweeted this:

Said Reddit thread (in r/fuckepic, “The premiere source for all Epic Games criticism”) can be viewed here.

Does that make the chart credible? Naturally, we reached out to Djundik and the Redditor who posted the charts to see if they still had the original documents. Their responses, respectively: “No” and (thus far) silence.

Let’s assume, for the sake of our collective sanity, that these figures are basically correct. They would suggest that with an effective commission rate probably somewhat beneath the 30 per cent baseline, and adjusted for costs, Steam handled perhaps $10bn of games sales in 2021.

Taken by itself, the chart indicates Steam had an operating margin of about 60 per cent and made $2bn of commission revenues, for about $1.3bn in profit just from Steam commissions in 2021.

If we assume that:

1) All Valve’s admin staff work on Steam (obviously untrue, and therefore conservative for per-head estimation purposes)

2) The numbers we’ve cited are roughly correct (not unfathomable)

It suggests Steam perhaps, maybe, possibly makes about $11.4mn per head in profit, per year, from commissions alone. Which is pretty spicy. For context, Wall Street money machine Jane Street can only boast a profit-per-head of $4.3mn. Even if you assume that the rest of Valve only breaks even, Steam’s cut from sales alone would mean the company as a whole makes nearly $3.9mn of profit per employee (higher than Citadel Securities, FWIW).

One thing that does perhaps support the chart’s credibility is how rapidly Valve’s lawyers moved to get the documents removed from the public docket.

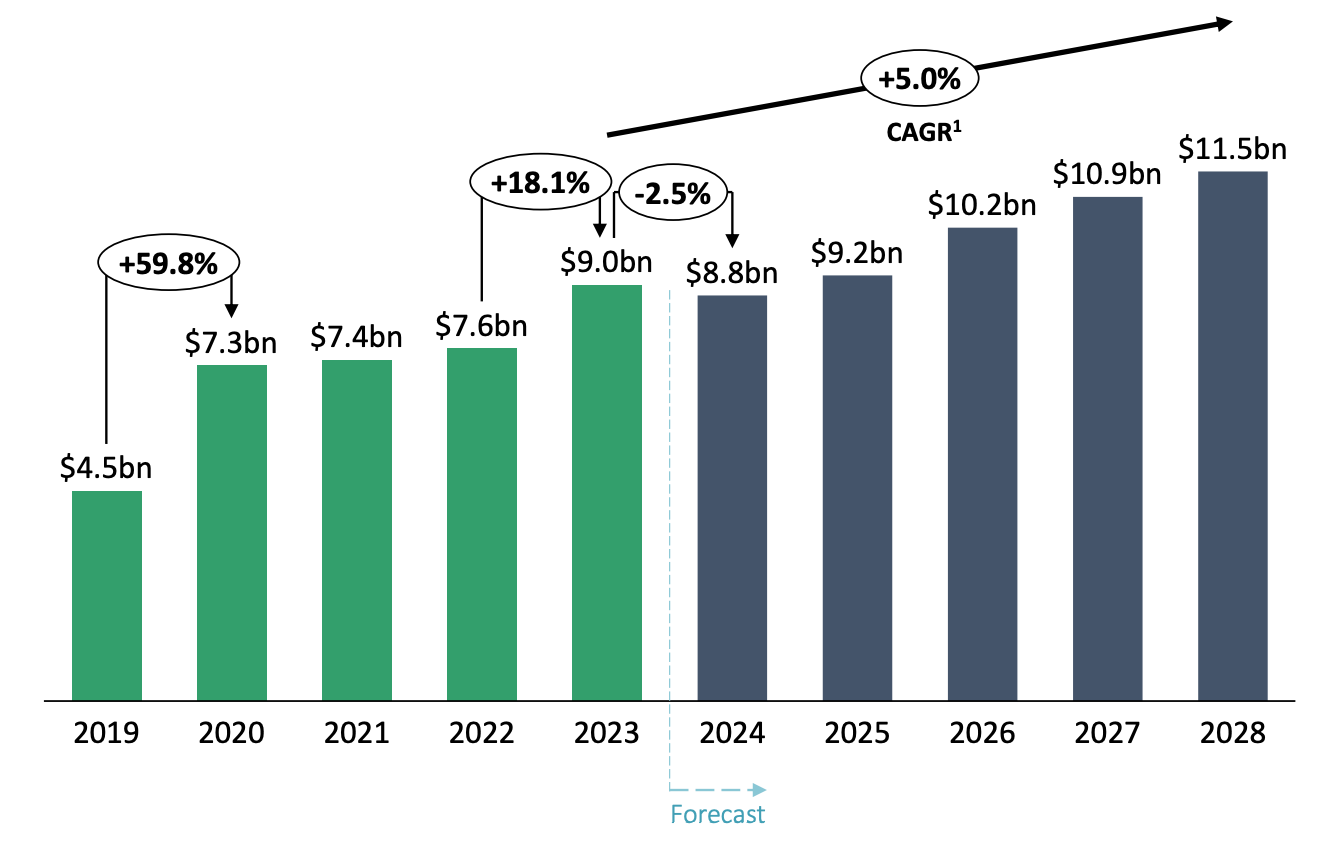

Filed in the court docket for the active class action is this chart, which projects that Steam’s overall revenues will pass $10bn next year (high-res):

No source is given in the filing, but the chart is taken from the Global PC Games Market Report 2024 by Video Game Insights, a market research group that has subsequently been bought by Sensor Tower.

In its methodology, VGI explains that those figures were derived from a mix of factors, including the number of reviews, how often certain games appear on user profiles, bestseller lists and “proprietary research”. Logically, we would expect this to include sales of Valve’s own games via Steam.

Like with most market research, it ought to be taken with a bucket of salt, although it’s at least in the same rough ballpark as an estimate by Microsoft that Valve as a whole made $6.5bn in revenue in 2021. Again, assuming these figures are even roughly true, what can they tell us?

Chiefly, it would indicate that commissions — despite being extremely lucrative — aren’t responsible for the majority of Steam’s overall revenues (if both disclosed charts, or Microsoft, are correct, we can compare $2bn in Steam commission income in 2021 to $6.5bn to $7.4bn of overall sales).

It’s tricky to believe. Sure, Valve likely makes chunky direct revenues for its own games, and associated microtransactions for things such as Counter-Strike “skins” — on which margins are likely to be excellent — but we’d suspect things are more tilted towards commissions.

Or, of course, that VGI’s figures — or any of the others we’ve seen — are just wrong. ¯\_(ツ)_/¯

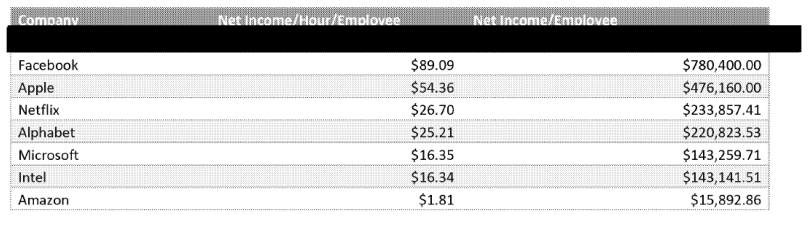

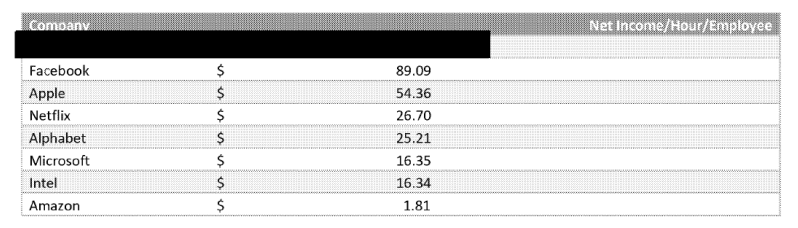

Hard profit figures remain elusive, but on overall revenues, at least, a court document from 2024 — shared by The GameDiscoverCo Newsletter — offers a teasing look inside the black box. In it, a heavily redacted email chain shows Valve employees discussing the company’s revenues per hour.

Kristian Miller, one of Valve’s data scientists, describes the company in the emails as a revenue “outlier”, sharing two charts that seem to put it above Silicon Valley’s top companies — possibly well above (high-res one and two):

In this, as with so many things, we invite readers to believe whatever it is they want to believe. If you work for Valve and want to tell us more, please get in touch. The company did not respond to our requests for comment on its financial performance or any other part of this article.

The prospect of a drawn-out court battle may mean more of the platform’s secrets spill out in the coming years. For now, Steam’s position — of an ultra-lucrative, efficient presence of a relatively small but healthy sector — seems secure. Yet as the games industry continues to grow, the temptation for a major tech company to take a serious swipe at it will only grow.

“Anybody who wants to put Valve out of business could do so, but nobody cares,” argues Michael Pachter, a gaming industry analyst at Wedbush Securities.

That said, it’s not like nobody has tried. Steam’s biggest rival is probably the Epic Games Store, which has been powered largely by the success of battle royale sensation Fortnite. Yet despite this huge draw, Epic “has failed to really impact Steam in any meaningful way”, according to Harding-Rolls:

This strategy has involved offering a better share of sales to developers and publishers and giving away lots of free games. This has prompted Steam to change its own revenue share policies. However, Steam continues to grow and is as dominant in terms of premium PC game sales as it has ever been. I think this illustrates that displacing Steam would be very challenging.

There are also several smaller distributors, such as Good Old Games — which made a sliver of profit on sales equivalent to about $55mn last year, and is owned by Poland’s CD Projekt — and indie platform Itch. Microsoft (which, in a different timeline, could surely have dominated this area) runs a somewhat unambitious store, while gaming heavyweight EA shut down Origin, its own launcher, earlier this year.

Visibility on market share across the sector is poor, but none, currently, seem to be approaching the reach and revenues of Steam.

Valve is a very weird company, and cheerfully admits it. Its 56-page Valve Handbook for New Employees lays out its unusual structure, and right at the start concedes that “it can take some time getting used to”.

And, pretty quickly, it’s made clear that Valve is indeed not like the other businesses:

Hierarchy is great for maintaining predictability and repeatability. It simplifies planning and makes it easier to control a large group of people from the top down, which is why military organizations rely on it so heavily.

But when you’re an entertainment company that’s spent the last decade going out of its way to recruit the most intelligent, innovative, talented people on Earth, telling them to sit at a desk and do what they’re told obliterates 99 percent of their value. We want innovators, and that means maintaining an environment where they’ll flourish.

That’s why Valve is flat. It’s our shorthand way of saying that we don’t have any management, and nobody “reports to” anybody else. We do have a founder/president, but even he isn’t your manager. This company is yours to steer — toward opportunities and away from risks. You have the power to green-light projects. You have the power to ship products.

The message is that Valve employees basically self-organise in what the company describes as a “flatland”, with even Newell (the “founder/president” referred to above) freed from hierarchical duties (the reality, according to one ex-insider, may be slightly less radical).

Flatness involves some interesting decisions. On a practical level, all desks at Valve have wheels, with staff physically shifting themselves around the office to be near the people they’re working with.

The handbook even includes a little illustration of how this should work:

Does this system produce results? On one level, yes: Valve seemingly makes loadsamoney. On another very visible level, absolutely not: Valve releases major new games at a glacial pace. The much-anticipated third title in the Half-Life series became the video game equivalent of Samuel Beckett’s Godot, until it was quietly cancelled.

“I’ve not met anybody who had a career there,” says Wedbush’s Pachter. “They all leave after, you know, 10 years. They last long enough to make money. But the developers I’ve known there have left for greener pastures because the company doesn’t publish games.”

Another oddity is the company’s use of “stack ranking”. Once a year, staff are asked to rank colleagues within their division based on skill level, productivity, group contribution and product contribution. These rankings are aggregated, and then used to determine compensation. As the handbook says:

By choosing these categories and basing the stack ranking on them, the company is explicitly stating, ‘This is what is valuable.’

This is potentially problematic, and not just from a financial planning perspective.

Whatever a company’s culture, it is bound to work for some people better than others. An investigation by YouTube channel People Make Games offers some interesting anecdata from people for whom it didn’t work, and explores the limitations of stack ranking (which, it suggests, rewards short-term, high-visibility work over less-glamorous, longer-term projects):

That’s not the only challenge. Valve presents itself as jocular, confident and unruffled, but the internet is a complicated place.

A report by the US’s Anti-Defamation League, published last year, claimed Steam’s forums were “rife with extremism & antisemitism”, with thousands of users deploying symbols such as the Nazi swastika, the sonnenrad and the Totenkopf. They found 1.18mn “potentially extremist” copypastas on Steam’s forums, with swastikas “by far” the most popular.

Their report suggests Valve has struggled — or ceased — to put a lid on such content:

A [ADL Centre on Extremish] analysis of copypastas on Steam also found evidence that Steam attempted to moderate certain extremist content before stopping for unknown reasons. From late 2019 through the height of the COVID-19 pandemic, when users in gaming spaces reached an all-time high, the use of several swastika copypastas sharply dropped to near-zero rates. The same swastika copypastas then sharply increased in frequency in September 2020, suggesting that Steam moderated this content for a brief period. There is no observable difference between the variations in copypasta posted prior to November 2019 and those posted after 2020.

Moderation issues are not unique to Steam, but Valve’s approach to handling such content on its platform is certainly laissez-faire.

In 2018, after a backlash, the company pulled the game Active Shooter — in which players could simulate a school shooting — from sale ahead of its release. In the wake of that decision, Steam outlined its philosophy for “who gets to be on the Steam store”. Its conclusion:

Valve shouldn’t be the ones deciding this. If you’re a player, we shouldn’t be choosing for you what content you can or can’t buy. If you’re a developer, we shouldn’t be choosing what content you’re allowed to create. Those choices should be yours to make…

With that principle in mind, we’ve decided that the right approach is to allow everything onto the Steam Store, except for things that we decide are illegal, or straight up trolling.

Conveniently, it’s the kind of libertarian approach that will probably make Valve the most money.

Valve is made in the image of Newell, who is most easily categorised as a libertarian. And there seems little argument that it has been a fantastic financial success.

Newell is 62 years old. It has been a few years since he gave a press interview, but an interesting profile of him published by Forbes last year said Newell was “rarely” in Valve’s offices any longer, no longer attended company events and had apparently since Covid-19 been living at sea in one of his five ships to avoid the virus.

Newell’s taste for the outlandish is not restricted to his life aquatic. Here’s what The Verge reported in May:

Valve co-founder and CEO Gabe Newell, the company behind Half-Life and DOTA 2 and Counter-Strike and preeminent PC game distribution platform Steam, has long toyed with the idea that your brain should be more connected to your PC. It began over a decade ago with in-house psychologists studying people’s biological responses to video games; Valve once considered earlobe monitors for its first VR headset. The company publicly explored the idea of brain-computer interfaces for gaming at GDC in 2019.

But Newell decided to spin off the idea. That same year, he quietly incorporated a new brain-computer interface startup, Starfish Neuroscience — which has now revealed plans to produce its very first brain chip later this year.

Speaking as part of a Valve-produced documentary about Half-Life, released last year (and not, apparently, on a boat at the time), Newell said:

I always have absolutely nothing interesting to say when people say ‘Would you reflect on your legacy?’. I really don’t look back a whole lot. I’m always excited by the future, right? So to me it’s like, I can look back at the things that we did, but to me they’re just the stepping stones to what we’re gonna be able to do in the future. That’s just how I’m wired.

While its founder takes strides towards becoming literally wired, Valve has settled in a strange spot. Under Newell’s leadership — geographically proximate or not — the company has been able to carve out and defend its own unusual niche, by doing things differently, and — for better and for worse — going where others have feared to tread.

But if he were ever to exit the picture, Valve would surely become a tempting takeover target. In the meantime, we hopefully have lots of fun legal discovery to look forward to, which might give us more information on the black hole of PC gaming.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}