Tools & Platforms

UBS Picks the Superior AI Stock to Buy After Earnings

The AI boom is nearly 3 years old, and one thing is certain about it: the boom has legs, and AI is here to stay. More and more companies are turning to the technology to enhance all sorts of functions, from customer service to chatbots to high-level data analytics and even to decision-making processes. According to Fortune Business Insights, up to 35% of all businesses have integrated AI into their work models.

-

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

This equals big money for the AI developers out there. Chip makers, AI app creators, data analysis firms – all of these and more have created an industry that was valued at $233 billion last year, and is estimated by Fortune Business Insights to hit $294 billion this year – and to show a CAGR of 29.2% through 2032, reaching $1.77 trillion that year. We should note that North American AI companies, mainly in the US, are leading this industry, with a 2024 market share of nearly 33%.

With numbers like these, it’s no surprise that UBS analysts are combing through the sector to pinpoint the most promising AI stocks. Their latest deep dive zeroes in on two recent earnings reporters – Palantir (NASDAQ:PLTR) and Advanced Micro Devices (NASDAQ:AMD) – to see which is the superior AI stock to buy. Let’s take a closer look.

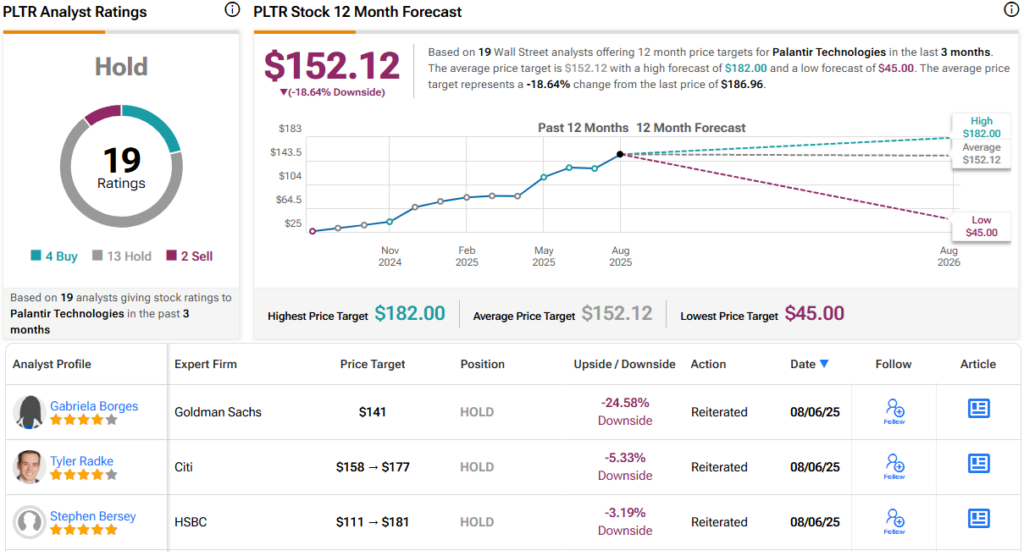

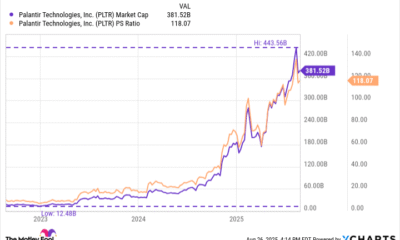

Palantir

The first AI stock we’ll look at here is one of the leaders in the field. Palantir is well-known for marrying AI technology and capabilities to the field of data analysis, a match that has matured into a solid product platform – AIP, or AI Platform – and a set of tools whose wide applicability has made them highly popular. Since its founding in 2003, Palantir has developed a reputation for innovation, and has built itself into a $441 billion giant of the AI industry.

Palantir’s AIP is purpose-built to combine AI tech with human intuition and flexibility, to gain the best from both – and to improve outcomes and results in data analysis. The products also use AI technology to improve the user interface, making it easy to use and simple to understand. The AI reads and responds in real text, based on natural language models; in practice, Palantir’s users don’t need to learn machine language or computer coding to communicate with the AI – they can simply enter their requests in clear text and receive responses the same way. The technology is also amenable to real-time translations, making Palantir’s products easy to market internationally – the system just needs to be told what language it is using, and its translation algorithms handle the rest.

Tools & Platforms

‘AI shame’ is a real phenomenon in the workplace, claims report; what may be ‘scaring’ top execs in America

A new survey from WalkMe, an SAP company, reveals a striking paradox in the modern workplace: The employees who use AI the most—top executives and Gen Z workers—are also the least likely to receive official guidance, training, or company approval for their use. The findings from the 2025 AI in the Workplace survey suggest that a phenomenon dubbed “AI shame” is taking hold. The annual survey polled 1,000 working U.S. adults who use AI in their jobs to understand the reality of AI adoption. Nearly half of all workers surveyed (48.8%) admitted to hiding their use of AI on the job to avoid judgment. This discomfort is particularly pronounced at the top, with 53.4% of C-suite leaders confessing they conceal their AI habits, despite being the most frequent users.x`Almost half (45%) of workers admit to pretending to know how to use an AI tool in a meeting to avoid scrutiny, while 49% have hidden their use of AI to avoid judgment. This trend is even more pronounced among Gen Z, with 55.5% pretending to understand AI tools and 62% hiding their use.

What makes Gen Z anxious about AI

Gen Z workers show both enthusiasm and anxiety regarding AI. A notable 62.6% of Gen Zers have used AI to complete work but then pretended it was their own, the highest rate among any generation. Over half (55.4%) have feigned understanding of AI in meetings.Despite this widespread use—89.2% of Gen Z employees use AI at work — they report receiving the least amount of support. Only 6.8% have received extensive, time-consuming AI training, and 13.5% received none at all. This lack of formal guidance has led 89.2% of them to use tools not provided or sanctioned by their employers.“Companies are not educating enough about this whole thing,” said Sharon Bernstein, WalkMe’s Chief Human Resources Officer, in an interview with Fortune. She noted that companies are failing to facilitate the use of AI tools or guide their employees effectively.

AI ‘Class Divide’ and Productivity Dilemma

The survey also points to an “AI class divide,” where access to training and guidance increases with rank. Only 3.7% of entry-level employees receive substantial training, compared to 17.1% of C-level executives. This leaves the most frequent users, junior and younger staff, to navigate the new technology on their own, risking a growing knowledge gap.While 80% of employees believe AI has boosted their productivity, a significant number are struggling. Almost 60% confessed to spending more time trying to manage AI tools than it would have taken to do the work themselves.Gen Z is particularly affected by this paradox:* 65.3% say AI slows them down, the highest among all age groups.* 68% feel pressure to produce more work because of it.* Nearly one in three are deeply anxious about AI’s impact on their jobs.This disconnect between corporate hype and on-the-ground reality fits into a broader picture of chaotic AI implementation. For instance, a recent MIT study found a staggering 95% failure rate for generative AI pilot programs at large enterprises, suggesting a significant gap between the theory of AI and its practical application.

Stethoscopes powered by artificial intelligence (AI) could help detect three different heart conditions in seconds, researchers say.

The original stethoscope, invented in 1816, allows doctors to listen to the internal sounds of a patient’s body.

But now a British team have designed one that can spot heart failure, heart valve disease and abnormal heart rhythms almost instantly.

The breakthrough AI-powered tool could be a “real game-changer” resulting in patients being treated sooner, the researchers say, with plans to roll the device out across the country.

The new device replaces the traditional chest piece with a device around the size of a playing card. It uses a microphone to analyse subtle differences in heartbeat and blood flow that the human ear cannot detect.

The study by Imperial College London and Imperial College Healthcare NHS Trust involved more than 200 GP surgeries in London.

More than 12,000 patients from 96 surgeries were examined with the AI stethoscope and were then compared to patients from 109 GP surgeries where the technology was not used.

Those examined with the device were 2.33 times more likely to be diagnosed with heart failure in the next 12 months, researchers said.

Abnormal heartbeat patterns, which have no symptoms but can increase stroke risk, were 3.5 times more detectable with the AI stethoscopes, while heart valve disease was 1.9 times more detectable.

Dr Sonya Babu-Narayan, clinical director at the British Heart Foundation (BHF) and consultant cardiologist, said: “This is an elegant example of how the humble stethoscope, invented more than 200 years ago, can be upgraded for the 21st century”.

Such innovations are vital “because so often this condition is only diagnosed at an advanced stage when patients attend hospital as an emergency”, she said.

“Given an earlier diagnosis, people can access the treatment they need to help them live well for longer.”

The findings have been presented to thousands of doctors at the European Society of Cardiology annual congress in Madrid, the world’s largest heart conference.

There are plans to roll out the new stethoscopes to GP practices in Wales, south London and Sussex.

Taco Bell’s chief digital officer says the company is having an “active conversation” about when to use and not to use AI.

The company has apparently rolled out voice AI-powered ordering at more than 500 drive-throughs, leading to unflattering viral moments like someone ordering 18,000 water cups in order to “bypass” the AI and get connected to a human server.

Chief Digital and Technology Officer Dane Matthews told The Wall Street Journal that even he has mixed experiences with technology: “Sometimes it lets me down, but sometimes it really surprises me.”

Overall, it sounds like Taco Bell is still deciding how broadly to deploy AI at the drive-through, with leeway for different franchisees to do things their own way. For example, rather than relying on AI exclusively, Matthews said it might make sense to have a human handle drive-through orders at busy restaurants with long lines.

“For our teams, we’ll help coach them: at your restaurant, at these times, we recommend you use voice AI or recommend that you actually really monitor voice AI and jump in as necessary,” he said.

-

Tools & Platforms3 weeks ago

Building Trust in Military AI Starts with Opening the Black Box – War on the Rocks

-

Ethics & Policy1 month ago

Ethics & Policy1 month agoSDAIA Supports Saudi Arabia’s Leadership in Shaping Global AI Ethics, Policy, and Research – وكالة الأنباء السعودية

-

Events & Conferences3 months ago

Events & Conferences3 months agoJourney to 1000 models: Scaling Instagram’s recommendation system

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoMumbai-based Perplexity Alternative Has 60k+ Users Without Funding

-

Funding & Business2 months ago

Funding & Business2 months agoKayak and Expedia race to build AI travel agents that turn social posts into itineraries

-

Education2 months ago

Education2 months agoVEX Robotics launches AI-powered classroom robotics system

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoHappy 4th of July! 🎆 Made with Veo 3 in Gemini

-

Business1 day ago

Business1 day agoThe Guardian view on Trump and the Fed: independence is no substitute for accountability | Editorial

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoOpenAI 🤝 @teamganassi

-

Mergers & Acquisitions2 months ago

Mergers & Acquisitions2 months agoDonald Trump suggests US government review subsidies to Elon Musk’s companies