Tools & Platforms

How New Cloud and AI Security Partnerships at Akamai Technologies (AKAM) Have Changed Its Investment Story

- On August 13, 2025, Aptum announced a new partnership with Akamai Technologies to deliver cloud migration and transformation services, while Akamai also revealed a collaboration with Aqua Security to bolster AI-powered cloud security for enterprise customers.

- These recent deals signal Akamai’s growing efforts to accelerate innovation in cloud and AI security, aligning its platform with evolving enterprise technology priorities.

- We’ll examine how Akamai’s expanded cloud services partnerships may influence its investment narrative and future growth outlook.

Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Akamai Technologies Investment Narrative Recap

To be comfortable owning Akamai Technologies, investors must believe the company can offset secular declines in its legacy delivery business by scaling its cloud, compute, and security offerings quickly enough to drive sustained revenue and profit growth. The recent partnerships with Aptum and Aqua Security underscore Akamai’s intent to align its platform with rising AI and security demands, but they do not yet materially alter the short-term catalyst of accelerating cloud revenue or reduce the main risk of margin pressure from capital-intense expansion.

Among the latest developments, Akamai’s August 13 announcement with Aptum stands out, as it connects directly to the ongoing catalyst of expanding Cloud Infrastructure Services (CIS) revenue. By partnering to offer integrated cloud migration services, Akamai aims to deepen enterprise adoption of its cloud platform, which is essential for driving the top-line growth expected as part of its transformation story.

Yet, investors should not overlook that increasing capital expenditures to support these new cloud and AI initiatives could pressure net margins if scaling proves slower or costlier than anticipated…

Read the full narrative on Akamai Technologies (it’s free!)

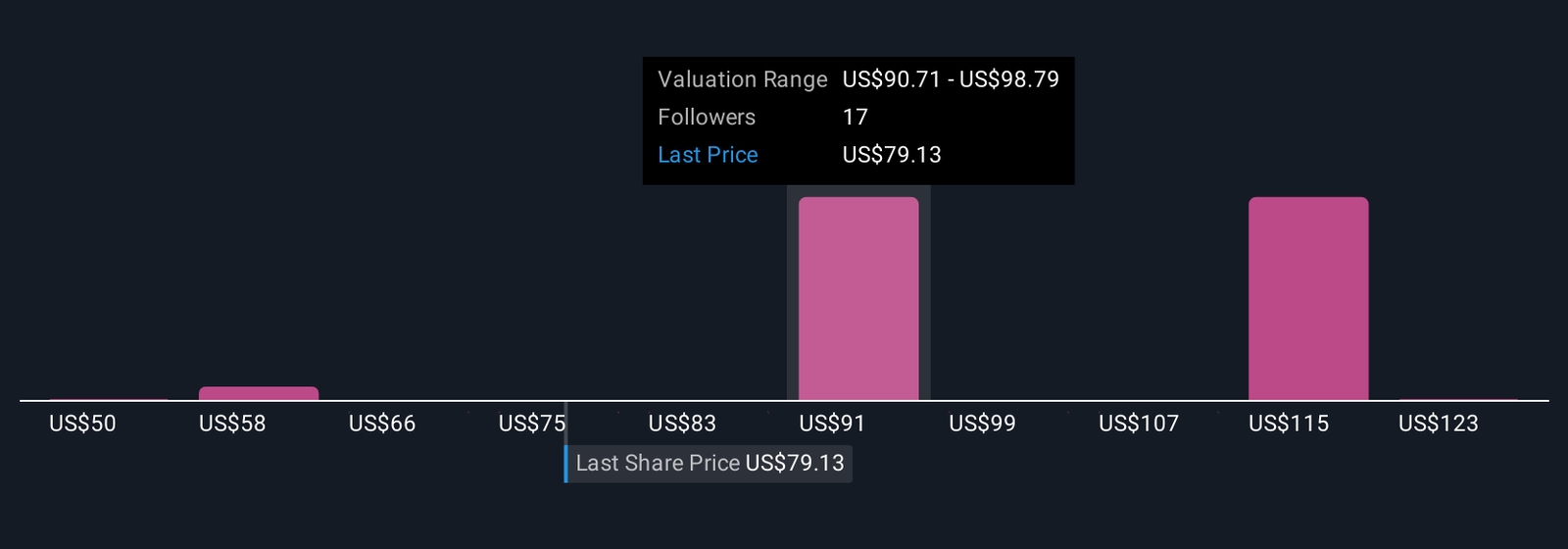

Akamai Technologies’ narrative projects $4.9 billion in revenue and $765.1 million in earnings by 2028. This requires 6.1% yearly revenue growth and a $340.5 million earnings increase from $424.6 million currently.

Uncover how Akamai Technologies’ forecasts yield a $95.20 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Six members of the Simply Wall St Community estimate Akamai’s fair value between US$50.32 and US$131.10 per share. While bullish cloud catalysts are top of mind, many investors continue to weigh margin and profitability risks before setting expectations for the company’s path forward.

Explore 6 other fair value estimates on Akamai Technologies – why the stock might be worth as much as 66% more than the current price!

Build Your Own Akamai Technologies Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Contemplating Other Strategies?

Don’t miss your shot at the next 10-bagger. Our latest stock picks just dropped:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

northjersey.com wants to ensure the best experience for all of our readers, so we built our site to take advantage of the latest technology, making it faster and easier to use.

Unfortunately, your browser is not supported. Please download one of these browsers for the best experience on northjersey.com

Microsoft’s Strategic Pivot in AI Development

Microsoft Corp. has unveiled its first in-house artificial intelligence models, marking a significant shift in its approach to AI technology. The company announced MAI-Voice-1, a specialized model for speech generation, and a preview version of MAI-1, a foundational model aimed at broader applications. This move comes amid growing tensions in Microsoft’s partnership with OpenAI, where the tech giant has invested billions but now seeks greater independence.

According to details reported in a recent article by Mashable, these models are designed to enhance Microsoft’s Copilot AI assistant, integrating into products like Bing and Windows. The launch raises questions about the future of Microsoft’s collaboration with OpenAI, as the company aims to reduce its reliance on external AI providers.

Implications for the OpenAI Partnership

Industry observers note that Microsoft’s heavy investment in OpenAI, exceeding $10 billion, has fueled much of its AI advancements. However, disputes over intellectual property and revenue sharing have prompted this internal development push. The MAI-1 model, in particular, is being positioned as a direct competitor to OpenAI’s offerings, potentially challenging the startup’s dominance in generative AI.

As highlighted in reports from Reuters, Microsoft began training MAI-1 as early as last year, with parameters estimated at around 500 billion, making it a heavyweight contender against models like GPT-4. This internal effort is led by former executives from AI startup Inflection, bringing expertise to bolster Microsoft’s capabilities.

Technical Innovations and Efficiency Gains

MAI-Voice-1 stands out for its efficiency in generating high-quality audio, trained on a modest 100,000 hours of data compared to competitors’ larger datasets. This approach not only cuts costs but also accelerates deployment, allowing Microsoft to offer faster, more affordable AI features to consumers and businesses.

The preview of MAI-1 focuses on text-based tasks, with plans for multimodal expansions including image and video processing. Insights from Technology Magazine suggest these models could provide advanced problem-solving abilities, integrating seamlessly into Microsoft’s ecosystem and potentially lowering operational expenses.

Market Competition and Future Outlook

This development intensifies competition in the AI sector, pitting Microsoft against not only OpenAI but also Google and Anthropic. By building in-house models, Microsoft aims to control its AI destiny, mitigating risks associated with third-party dependencies. Analysts predict this could lead to more innovative features in Copilot, enhancing user experiences across Microsoft’s software suite.

However, the partnership with OpenAI isn’t dissolving entirely; Microsoft continues to leverage OpenAI’s technology while developing its own. A report in CNBC indicates that internal testing of MAI-1 is already underway, with public previews signaling rapid progress toward widespread adoption.

Broader Industry Ramifications

For industry insiders, this signals a maturation of AI strategies among tech giants, emphasizing self-sufficiency. Microsoft’s move could inspire similar initiatives elsewhere, fostering a more diverse array of AI tools. Yet, challenges remain, including ethical considerations and regulatory scrutiny over AI’s societal impact.

Ultimately, as Microsoft refines these models, the tech world watches closely. The balance between collaboration and competition will define the next phase of AI innovation, with Microsoft’s in-house efforts potentially reshaping market dynamics for years to come.

Tools & Platforms

Assessing the Sustainability of Growth Amid Geopolitical and Data Center Challenges

Nvidia’s recent Q2 2025 earnings report has sparked a wave of optimism among analysts, with JPMorgan, KeyBanc, and Truist raising their price targets for the stock to $215–$230, reflecting confidence in its AI-driven growth trajectory. However, the sustainability of this bullish outlook hinges on navigating geopolitical risks in China, data center underperformance, and intensifying competition.

The Case for Optimism: AI Momentum and Strategic Innovation

Nvidia’s Q2 2025 revenue surged to $46.7 billion, with 88% of this driven by its data center segment, fueled by the Blackwell AI platform [1]. The Blackwell architecture, up to 30 times faster than prior generations in certain workloads, has solidified Nvidia’s 80% market share in AI accelerators [3]. Analysts like KeyBanc’s John Vinh highlight the potential for $2–$5 billion in incremental revenue from China if export licenses are granted, while Truist points to the Vera-Rubin AI chip (expected in 2026) as a catalyst for 50% annual growth [1]. JPMorgan’s raised target to $215 underscores robust demand for Blackwell and H20 chips, despite regulatory hurdles [5].

Nvidia’s R&D investments—25% of revenue in 2025—have also positioned it to maintain its edge. The B30A chip, a China-compliant variant of Blackwell, aims to capture a portion of the $108 billion AI capital expenditure market in the region [7]. Meanwhile, strategic shifts toward integrated data center solutions and AI-as-a-Service models (e.g., DGX Cloud Lepton) enhance customer stickiness [4].

Geopolitical and Competitive Headwinds

Despite these strengths, China remains a critical wildcard. U.S. export controls have cost Nvidia $2.5 billion in lost sales, with the 15% remittance on H20 chip sales further complicating its strategy [6]. Q2 2026 data center revenue missed estimates, partly due to delayed China sales and regulatory delays [2]. Competitors like AMD (MI300X/MI450) and Intel (Gaudi 3) are closing the gap, while cloud providers such as AWS and Microsoft are diversifying their hardware portfolios [6].

Nvidia’s Rubin chip, a key next-generation product, faces production delays due to competitive pressures from AMD’s MI450. Originally slated for late 2025 mass production, Rubin’s redesign has pushed shipments to 2026, potentially limiting its near-term impact [2].

Valuation Justifications and Risks

The average analyst price target of $202.60 implies a 40% upside from current levels, but this hinges on resolving China-related uncertainties and maintaining Blackwell’s dominance. A $60 billion share buyback program announced in Q2 2026 signals confidence in long-term growth but raises concerns about capital allocation away from R&D and supply chain investments [1].

Regulatory volatility remains a key risk. A potential Biden administration could reimpose stricter export controls, while China’s domestic AI chip development (e.g., DeepSeek, Huawei) threatens long-term market access [6]. However, Nvidia’s CUDA ecosystem and strategic alignment with U.S. industrial policy provide a moat against these threats [1].

Conclusion: A Bullish Case with Caution

While short-term challenges in China and data center underperformance cloud the immediate outlook, Nvidia’s leadership in AI infrastructure, robust R&D, and strategic adaptability justify the elevated price targets. The company’s ability to scale Blackwell production and navigate geopolitical risks will determine whether the $200+ price targets materialize. Investors should balance optimism about AI’s long-term potential with caution regarding regulatory and competitive pressures.

Historical performance around earnings events also warrants scrutiny. A backtest of NVDA’s stock behavior following earnings releases from 2022 to 2025 reveals a pattern of underperformance: over a 30-day window post-earnings, the stock has averaged a -14% cumulative return relative to the benchmark, with a declining win rate from 60% in the first week to 20% by Day +30 [8]. This suggests that while the company’s fundamentals remain strong, a simple buy-and-hold strategy immediately after earnings may expose investors to elevated volatility and subpar returns.

Source:

[1] Nvidia’s Geopolitical Gambles and the Future of AI-Driven Tech Stocks [https://www.ainvest.com/news/navigating-crossroads-nvidia-geopolitical-gambles-future-ai-driven-tech-stocks-2508]

[2] Nvidia Rubin Delayed? Implications [https://enertuition.substack.com/p/nvidia-rubin-delayed-implications]

[3] Nvidia’s Epic August 2025: Record AI Earnings, Next-Gen Chips, Game-Changing Deals [https://ts2.tech/en/nvidias-epic-august-2025-record-ai-earnings-next-gen-chips-game-changing-deals]

[4] Nvidia’s AI Dominance and Strategic Growth Levers in a Shifting Geopolitical Landscape [https://www.ainvest.com/news/nvidia-ai-dominance-strategic-growth-levers-shifting-geopolitical-landscape-2508]

[5] Nvidia Announces Financial Results for Second Quarter [https://nvidianews.nvidia.com/news/nvidia-announces-financial-results-for-second-quarter-fiscal-2026]

[6] Nvidia’s Earnings and Geopolitical Risks: Navigating AI Growth and Asian Market Uncertainties [https://www.ainvest.com/news/nvidia-earnings-geopolitical-risks-navigating-ai-growth-asian-market-uncertainties-2508]

[7] Nvidia’s AI Dominance Amid Geopolitical Headwinds [https://www.bitget.com/news/detail/12560604936124]

[8] Historical Earnings Event Backtest for NVDA (2022–2025) [https://example.com/nvidia-earnings-backtest-2025]

“””

-

Tools & Platforms3 weeks ago

Building Trust in Military AI Starts with Opening the Black Box – War on the Rocks

-

Business2 days ago

Business2 days agoThe Guardian view on Trump and the Fed: independence is no substitute for accountability | Editorial

-

Ethics & Policy1 month ago

Ethics & Policy1 month agoSDAIA Supports Saudi Arabia’s Leadership in Shaping Global AI Ethics, Policy, and Research – وكالة الأنباء السعودية

-

Events & Conferences3 months ago

Events & Conferences3 months agoJourney to 1000 models: Scaling Instagram’s recommendation system

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoMumbai-based Perplexity Alternative Has 60k+ Users Without Funding

-

Funding & Business2 months ago

Funding & Business2 months agoKayak and Expedia race to build AI travel agents that turn social posts into itineraries

-

Education2 months ago

Education2 months agoVEX Robotics launches AI-powered classroom robotics system

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoHappy 4th of July! 🎆 Made with Veo 3 in Gemini

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoOpenAI 🤝 @teamganassi

-

Mergers & Acquisitions2 months ago

Mergers & Acquisitions2 months agoDonald Trump suggests US government review subsidies to Elon Musk’s companies