AI Insights

After Plummeting Over $1 Trillion in Value, This Super Artificial Intelligence (AI) Stock Is Mounting a Major Comeback, With Analysts Predicting Gains of Up to 400%

Earlier this year, Nvidia lost more than $1 trillion in market capitalization. Now, it’s the most valuable company in the world.

For a few years now, the artificial intelligence (AI) movement has largely hinged on the performance of a single company: Nvidia (NVDA -0.42%).

Sure, if Microsoft or Amazon posted strong results from their respective cloud computing platforms or if Tesla managed to hype investors up over the prospects of self-driving robotaxis or humanoid robots, the technology sector might see a fleeting upward movement. At the end of the day, however, the focus seemed to eventually return to Nvidia — with analysts obsessing over how demand for the company’s chips and data center services were trending.

During the first half of the year, Nvidia’s ship was caught in an epic storm. Investors started to question the company’s long-growth prospects — inspiring prolonged periods of panic-selling in the process. All told, Nvidia’s market cap dropped by more than $1 trillion.

But now, with a market value north of $4 trillion, Nvidia has reclaimed its position as the most valuable company on the planet. Even better? Some on Wall Street are calling for further gains of up to 400%.

Let’s explore the tailwinds supporting Nvidia’s long-term growth narrative and detail why Wall Street sees such massive upside for the king of the chip realm.

One Wall Street analyst is calling for a $10 trillion valuation for Nvidia

One of the most bullish Nvidia analysts on Wall Street is the I/O Fund’s Beth Kindig. Kindig suggested that Nvidia could reach a $10 trillion market cap by 2030 — implying 140% upside from current levels. Let’s explore the main catalysts supporting Kindig’s forecast.

According to management from Microsoft, Amazon, and Alphabet, roughly $260 billion will be spent in 2025 alone on AI infrastructure. On top of that, Meta Platforms is expected to spend roughly $70 billion on capital expenditures this year — nearly double what it spent in 2024. Lastly, Oracle is beginning to make significant headway in infrastructure services — allowing companies to rent Nvidia GPUs from their cloud-based data center platform. From a macro perspective, rising capex from the cloud hyperscalers bodes well for chip demand.

Kindig takes these secular tailwinds one step further, suggesting that competition from Intel and Advanced Micro Devices does not pose much of a threat to Nvidia’s dominance. While it’s hard to know how vendor preferences could change over the next several years, current industry research trends suggest that Kindig might be right — underscored by Nvidia’s rising market share in the AI accelerator industry.

The area of Kindig’s analysis that I think is currently overlooked the most revolves around Nvidia’s software architecture, called CUDA. Since CUDA is integrated tightly with Nvidia’s hardware, developers essentially become locked into the company’s ecosystem.

Not only does this lead to customer stickiness, but it opens the door for Nvidia to be at the forefront of more sophisticated, evolving AI applications in areas such as robotics and autonomous driving.

Image source: Getty Images.

What about $20 trillion?

Former management consulting executive Phil Panaro is even more bullish than Kindig. By 2030, Panaro thinks Nvidia’s share price could reach $800 — implying roughly a $20 trillion market cap.

Panaro cites opportunities across Web3 development and evolving use cases around how enterprises and governments leverage AI to generate more efficiency and cost savings as the main pillars supporting Nvidia’s upside.

While these trends could eventually drive significant demand for Nvidia’s data center services, tech adoption within the government tends to move slowly. Meanwhile, Web3 remains an emerging concept that could take far longer to mature than Panaro is assuming.

Is Nvidia stock a buy right now?

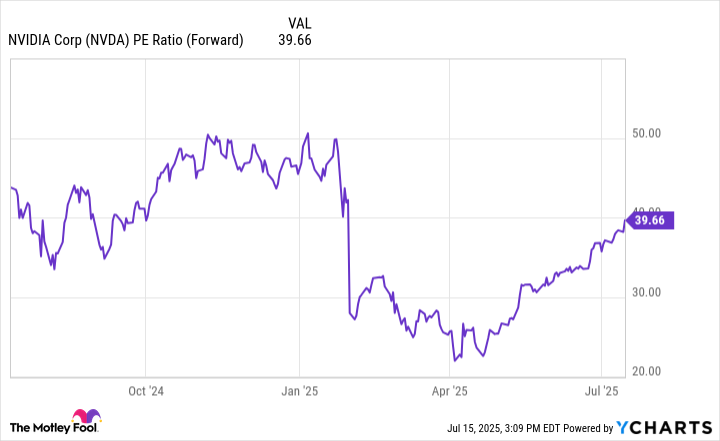

Nvidia stock has been mounting an epic comeback over the last couple of months. This valuation expansion can be easily seen through the dynamics of the company’s rising forward price-to-earnings (P/E) multiple. Nevertheless, Nvidia’s forward P/E of 40 is still well below levels seen earlier this year.

NVDA PE Ratio (Forward) data by YCharts

Trying to model Nvidia’s peak valuation is an exercise in false precision. The bigger takeaway is that analysts on Wall Street are not only calling for significant upside in the stock, but they have outlined the foundation for Nvidia’s long-term growth. The important theme here is that Nvidia has opportunities well beyond selling chips — many of which have yet to make meaningful contributions to the business.

I see Nvidia stock as a no-brainer. Investors with a long-run time horizon might consider scooping shares up at current prices and plan to hold on for years to come.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Intel, Meta Platforms, Microsoft, Nvidia, Oracle, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft, short August 2025 $24 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

“Attackers conceal instructions via ultra-small fonts, background-matched text, ASCII smuggling using Unicode Tags, macros that inject payloads at parsing time, and even file metadata (e.g., DOCX custom properties, PDF/XMP, EXIF),” Granoša explained. “These vectors evade human review yet are fully parsed and executed by LLMs, enabling indirect prompt injection.”

Countermeasures

Justin Endres, head of data security at cybersecurity vendor Seclore, argued that security leaders can’t rely on legacy tools alone to defend against malicious prompts that turn “everyday files into Trojan horses for AI systems.”

“[Security leaders] need layered defenses that sanitize content before it ever reaches an AI parser, enforce strict guardrails around model inputs, and keep humans in the loop for critical workflows,” Endres advised. “Otherwise, attackers will be the ones writing the prompts that shape your AI’s behavior.”

This semiconductor and networking specialist is a force to be reckoned with in the artificial intelligence (AI) space.

Since the dawn of the artificial intelligence (AI) era, a number of players have been at the leading edge of the technology. Perhaps no company has exemplified the vast potential of AI more than Nvidia (NVDA 3.91%). Since early 2023, the chipmaker’s stock has surged more than 1,000% (as of this writing) as its graphics processing units (GPUs) have become the gold standard for facilitating the technology.

However, investors may be surprised to learn that Broadcom (AVGO 10.07%) has actually outperformed Nvidia over the past year, as its stock has soared 149% compared with 63% for Nvidia. Furthermore, several pronouncements by the company during its recent quarterly report suggest that trend is poised to continue.

Let’s look at what’s driving Broadcom’s robust rally and why I predict the company is on track to be the next Nvidia.

Image source: Getty Images.

The next big winner

Nvidia’s GPUs have transformed AI by providing the massive computational horsepower required to power AI models. These lightning-fast chips offer extremely flexible use cases and are unmatched for this purpose, which is why Nvidia has thrived over the past few years.

It’s also no surprise that Broadcom has benefited from the accelerating adoption of AI, as the company’s Ethernet switching and networking products have long been a staple in data centers. However, Broadcom’s application-specific integrated circuits (ASICs) have been gaining ground. These custom-designed AI accelerators, which Broadcom calls XPUs, are tailored to specific tasks and therefore more energy efficient. Rapid adoption of this chips has fueled a blistering run for Broadcom stock, which is up more than 500% since early 2023, earning its membership in the $1 trillion club.

In the third quarter, Broadcom generated record revenue that accelerated 22% year over year to $15.9 billion, resulting in adjusted earnings per share (EPS) that jumped 36% to $1.69. The company was clear that it was AI that was driving this train, as its AI-specific revenue accelerated 63% year over year to $5.2 billion. The results were well ahead of Wall Street’s expectations, as analysts’ consensus estimates called for revenue of $15.82 billion and adjusted EPS of $1.66.

For context, in its fiscal 2026 second quarter (ended July 27), Nvidia’s data center segment, driven primarily by AI, grew 56% year over year, down from 73% growth in Q1, which shows its growth is decelerating.

However, it was management’s commentary that gave investors cause to celebrate, as Broadcom delivered two pieces of news that bode well for the future.

First, Broadcom stated that it continues to expand its business with its three biggest hyperscale customers. While the company doesn’t disclose who these customers are, they are widely believed to be Alphabet, Meta Platforms, and TikTok parent ByteDance. During the conference call to discuss the results, CEO Hock Tam said, “We continue to gain share at our three original customers.” He went on to say the company is forecasting its AI-centric growth to be higher next year, accelerating compared to the 50% to 60% growth it expects in 2025.

The other big development was that Broadcom confirmed the addition of a fourth big hyperscale customer, which many analysts believe to be OpenAI. The company said this new client moved from prospect to “qualified customer,” and had approved production of “AI racks based on our XPUs.” As a result, Broadcom boosted its backlog by $10 billion to $110 billion.

The next Nvidia?

Wall Street’s reaction to Broadcom’s results was decidedly bullish, as no fewer than 16 analysts boosted their price targets on the stock. Many of these cited the accelerating demand for Broadcom’s ASICs as a factor.

Ben Reitzes of Melius Research views Broadcom as a “Magnificent Eight” stock, arguing that it should be added to the Magnificent 7 stocks. He goes on to say that he has long believed that Nvidia’s share would fall over time, with Broadcom eventually taking a roughly 30% share of the AI compute market.

That said, Reitzes also believes that a rising tide lifts all boats, and both companies will be massive winners as the adoption of AI continues to gain steam. That said, the analyst points out that over the long term, Nvidia’s CUDA programming library shouldn’t be underestimated, as this software ecosystem is favored by developers and provides Nvidia with a significant competitive advantage.

So while Broadcom will likely be the next Nvidia, the demand for AI continues to climb, and the market will be able to support two major players, so Nvidia and Broadcom will likely both be market-beating investments from here.

From a valuation perspective, the recent spike in Broadcom’s stock price has seen a commensurate increase in its multiple. Broadcom stock is currently selling for 37 times next year’s earnings, compared to 27 for Nvidia. Both are trading for a premium, but both are also well-positioned to profit from the growing adoption of AI.

Danny Vena has positions in Alphabet, Broadcom, Meta Platforms, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Meta Platforms, and Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Artificial intelligence (AI) is rapidly transforming clinical care, offering healthcare leaders new tools to improve workflows through automation and enhance patient outcomes with more accurate diagnoses and personalized treatments. This resource provides a framework for understanding how AI is applied across the patient journey, from pre-visit interactions to post‑visit monitoring and ongoing care. It focuses on actionable use cases to help healthcare organizations evaluate AI technologies holistically, balance innovation with feasibility, and navigate the evolving landscape of AI in healthcare.

For a deeper exploration of any specific use case featured in this infographic, check out our comprehensive compendium. It offers detailed insights into these technologies, including their benefits, implementation considerations, and evolving role in healthcare.

-

Business2 weeks ago

Business2 weeks agoThe Guardian view on Trump and the Fed: independence is no substitute for accountability | Editorial

-

Tools & Platforms4 weeks ago

Building Trust in Military AI Starts with Opening the Black Box – War on the Rocks

-

Ethics & Policy2 months ago

Ethics & Policy2 months agoSDAIA Supports Saudi Arabia’s Leadership in Shaping Global AI Ethics, Policy, and Research – وكالة الأنباء السعودية

-

Events & Conferences4 months ago

Events & Conferences4 months agoJourney to 1000 models: Scaling Instagram’s recommendation system

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoMumbai-based Perplexity Alternative Has 60k+ Users Without Funding

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoHappy 4th of July! 🎆 Made with Veo 3 in Gemini

-

Education2 months ago

Education2 months agoVEX Robotics launches AI-powered classroom robotics system

-

Education2 months ago

Education2 months agoMacron says UK and France have duty to tackle illegal migration ‘with humanity, solidarity and firmness’ – UK politics live | Politics

-

Funding & Business2 months ago

Funding & Business2 months agoKayak and Expedia race to build AI travel agents that turn social posts into itineraries

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoOpenAI 🤝 @teamganassi