Tools & Platforms

A Hidden Catalyst in the AI Boom

The artificial intelligence (AI) revolution is no longer a distant promise—it’s a present-day reality. At the forefront of this transformation is Nvidia, whose dominance in AI chips has made it a household name. Yet, beneath the spotlight of its GPUs lies a subtler but equally critical shift: the redefinition of AI infrastructure. By acquiring AI startups, investing in cloud partnerships, and expanding domestic manufacturing, Nvidia is not just building a chip empire—it’s reshaping the entire ecosystem. For investors, this signals an opportunity to look beyond the GPU spotlight and uncover underappreciated players like Micron Technology, whose role in AI infrastructure is poised to deliver outsized returns.

The Nvidia Effect: From Chips to Ecosystems

Nvidia’s 2025 acquisitions—Gretel, Lepton AI, and CentML—highlight its strategy to control the full AI stack. Gretel’s synthetic data tools address privacy and data scarcity, while Lepton AI’s GPU rental platform democratizes access to AI compute. CentML’s optimization software ensures these models run efficiently on Nvidia hardware. These moves are not isolated; they reflect a broader trend. In 2024 alone, Nvidia participated in 49 funding rounds for AI startups, including $100 million in OpenAI’s $6.6 billion round and $1.05 billion in Wayve’s autonomous driving venture.

Nvidia’s investments are not just about financial returns—they’re about ecosystem control. By backing startups that enhance data quality, cloud accessibility, and model efficiency, Nvidia ensures its GPUs remain the backbone of AI innovation. This strategy is amplified by its domestic manufacturing partnerships with TSMC, Foxconn, and Wistron, which aim to produce $500 billion in AI infrastructure over four years. The result? A self-reinforcing cycle where Nvidia’s hardware, software, and cloud partnerships lock in market share.

The Hidden Catalyst: Micron Technology’s AI Infrastructure Play

While Nvidia grabs headlines, Micron Technology operates in the shadows of the AI boom. As a supplier of high-bandwidth memory (HBM), Micron’s HBM3E chips are critical for AI training and inferencing. These chips power Nvidia’s Blackwell Ultra B300 GPU and its upcoming GB200 and GB300 systems. What sets Micron apart is its technological edge: its 12-high HBM3E design offers 50% more memory capacity than SK Hynix’s 8-high version, while reducing power consumption by 30%.

Micron’s financials underscore its strategic importance. In Q2 2025, the company reported non-GAAP diluted EPS of $1.56, with operating margins at 24.9% and EBITDA margins at 50.7%. HBM gross margins of 50–55%—well above industry averages—reflect its premium positioning. Data center revenue now accounts for over half of Micron’s total revenue, a testament to surging demand for AI memory. For fiscal 2025, Micron raised its revenue guidance to $11.1–$11.3 billion, with non-GAAP EPS projected to jump 141% year-over-year.

Why Micron Is Undervalued—and Why That’s a Problem

Despite these strengths, Micron trades at a forward P/E of 10, significantly lower than the Nasdaq-100’s 30. This undervaluation stems from market myopia: investors fixate on AI chipmakers like Nvidia and AMD while overlooking the memory and storage layer. Yet, the HBM market is projected to grow from $4 billion in 2023 to $130 billion by 2033, with Micron capturing 24% of the market by year-end.

Micron’s partnerships with Nvidia and AMD are further cementing its role. Its HBM3E is already in production for next-gen AI systems, and its $14 billion capex plan for 2025—funded by new facilities in Idaho and Singapore—positions it to meet surging demand. Additionally, its $150 billion U.S. manufacturing commitment aligns with global supply chain resilience trends, making it a strategic partner for hyperscalers like Microsoft and Amazon.

The Investment Case: Balancing Risk and Reward

For investors, the key is to balance Nvidia’s visibility with Micron’s potential. While Nvidia’s $100 billion market cap and $100 million OpenAI investment signal its dominance, Micron’s $70 billion valuation offers a more compelling risk-reward profile. Its HBM market share growth, 50%+ gross margins, and alignment with AI’s infrastructure needs make it a high-conviction play.

However, risks persist. The HBM market is capital-intensive, and Micron’s $14 billion capex could strain short-term margins. Additionally, geopolitical tensions and supply chain disruptions could impact its U.S. manufacturing plans. Yet, these risks are mitigated by Micron’s technological leadership and long-term contracts with AI leaders.

Conclusion: Look Beyond the GPU Spotlight

Nvidia’s strategic acquisitions and investments are more than a corporate strategy—they’re a blueprint for the future of AI. By controlling the ecosystem, from data to cloud to hardware, Nvidia ensures its dominance. But for investors seeking alpha, the real opportunity lies in the underappreciated players like Micron. As AI adoption accelerates, the demand for HBM and memory solutions will outpace even the most bullish GPU forecasts. Micron’s undervalued stock, robust financials, and critical role in AI infrastructure make it a compelling addition to any portfolio.

In the AI arms race, the winners won’t just be the chipmakers—they’ll be the enablers. And Micron, with its HBM3E and strategic vision, is ready to lead.

UNIVERSITY PARK, Pa. — Teaching and Learning with Technology at Penn State is enrolling faculty and staff until Sept. 30 in the Provost Endorsement Program: AI-Enhanced Pedagogy, which will be held during the fall 2025 semester. Participants will explore and integrate generative AI technologies into their teaching practices.

To complete the endorsement program, participants must attend seven internal Penn State events related to generative AI in instruction during the fall 2025 semester. Events will vary between in person and online options. Events will be offered by experts from Teaching and Learning with Technology, Commonwealth Campus instructional designers, the University Libraries, and the Schreyer Institute for Teaching Excellence.

Additionally, participants will use Canvas to submit a revised assignment, an insights post, and a philosophy video to receive individualized feedback from the endorsement program leads.

The goals of this endorsement program are to support the discovery of generative AI teaching and learning opportunities as a University-wide community and to support the tailoring of GenAI uses to enhance student skills development.

By completing this endorsement program, participants will:

- Identify teaching and/or learning opportunities for equity, ethical practices or disciplinary skills afforded by generative AI technologies.

- Explore and use at least three generative AI tools.

- Review and revise a course or teaching approach with generative AI to support student success.

- Create a video of an instructional philosophy with generative AI that could be given to students.

Faculty and staff can find more information and enroll on the AI-Enhanced Pedagogy webpage.

- DXC Technology recently announced partnerships with startups Acumino, CAMB.AI, and GreenMatterAI to advance AI solutions in the automotive and manufacturing industries, focusing on smart factory robotics, real-time speech translation, and synthetic data projects.

- This collaboration, made as part of the STARTUP AUTOBAHN initiative, highlights DXC’s commitment to transforming emerging technology into practical industry impact by accelerating AI adoption.

- We’ll examine how these new AI partnerships could reshape DXC Technology’s investment narrative and long-term prospects in digital transformation.

Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

DXC Technology Investment Narrative Recap

To be a shareholder in DXC Technology today, you need to believe that the company’s efforts in digital transformation and AI can counter persistent revenue declines and revive organic growth. While the new partnerships with Acumino, CAMB.AI, and GreenMatterAI showcase momentum in AI, the immediate effect on stabilizing short-term revenues or addressing the ongoing decline in the GIS segment is likely to be modest, given the inherent scale and timing of these projects.

Of recent announcements, DXC’s deal to create the DXC Agentic Security Operations Center with 7AI stands out as especially relevant alongside the new automotive and manufacturing AI partnerships. This reflects a deepening focus on expanding digital offerings through AI-driven solutions, which underpins the most important catalyst for the stock: improved client demand and bookings growth from digital modernization, even as near-term performance remains pressured.

However, investors should not overlook that, despite these innovation efforts, persistent challenges in revenue and margin stabilization continue to weigh on the company’s outlook, especially if…

Read the full narrative on DXC Technology (it’s free!)

DXC Technology’s outlook projects $12.1 billion in revenue and $208.6 million in earnings by 2028. This implies a 1.7% annual revenue decline and a $170.4 million decrease in earnings from the current $379.0 million.

Uncover how DXC Technology’s forecasts yield a $15.12 fair value, in line with its current price.

Exploring Other Perspectives

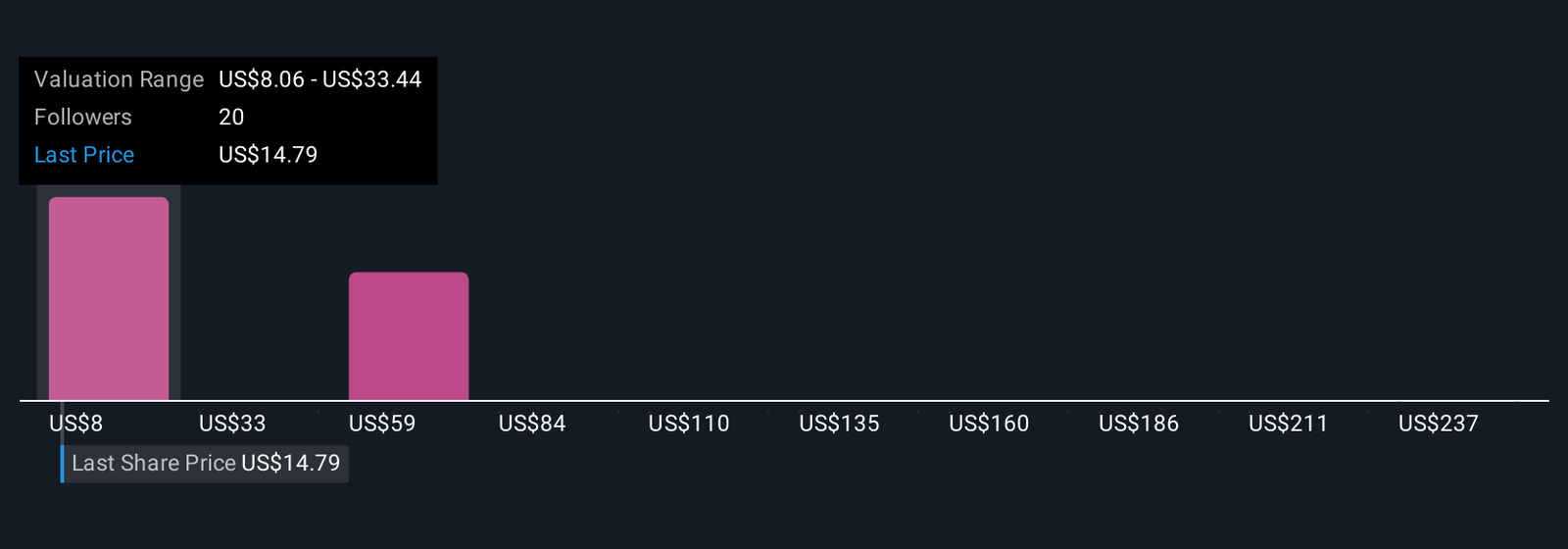

Six Simply Wall St Community members estimate DXC’s fair value between US$8.06 and US$261.89, indicating significant differences in growth assumptions. Balance these viewpoints with persistent risks to revenue and backlog conversion that could impact near-term earnings and investor sentiment.

Explore 6 other fair value estimates on DXC Technology – why the stock might be worth 46% less than the current price!

Build Your Own DXC Technology Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Interested In Other Possibilities?

Opportunities like this don’t last. These are today’s most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Tools & Platforms

Will Sea Dagger’s AI-Driven Tech Shift Leidos Holdings’ (LDOS) Role in Government Defense Contracts?

- Leidos recently unveiled the Sea Dagger, a next-generation Commando Insertion Craft for the Royal Navy, featuring high speed, modular mission systems, and autonomous technologies tailored for modern maritime operations.

- This unveiling positions Leidos as a prominent innovator in advanced maritime defense solutions, aligning with major UK and AUKUS defense modernization priorities.

- We’ll explore how the Sea Dagger launch, leveraging autonomy and AI, could shape Leidos Holdings’ government contract growth outlook.

Trump’s oil boom is here – pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Leidos Holdings Investment Narrative Recap

To be a shareholder in Leidos Holdings, you need confidence in the company’s ability to capture long-term government spending on defense modernization and advanced technology, while managing its reliance on large public sector contracts. The announcement of Sea Dagger enhances Leidos’ credentials in maritime autonomy and aligns with top spending priorities, but gives only an incremental boost to near-term government contract momentum, which remains the company’s key catalyst. The largest risk continues to be shifts in government funding priorities, which could disrupt expected revenue growth if budgets tighten.

Among recent developments, Leidos winning a $128 million FBI task order for agile software development illustrates how its expertise in secure, high-tech government solutions is translating into new business opportunities. This aligns with the same digital innovation and defense modernization themes seen in the Sea Dagger project, further supporting the company’s biggest catalyst: continued multi-year growth in national security and technology contracts.

Yet, despite these advances, if defense spending priorities change faster than expected, investors need to be aware that…

Read the full narrative on Leidos Holdings (it’s free!)

Leidos Holdings is projected to reach $18.6 billion in revenue and $1.5 billion in earnings by 2028. This outlook requires a 3.0% annual revenue growth rate and a $0.1 billion increase in earnings from the current $1.4 billion.

Uncover how Leidos Holdings’ forecasts yield a $186.69 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Eight fair value estimates from the Simply Wall St Community range from US$102 to US$285.81. While high expectations for government modernization support optimism, investor forecasts remind you opinions vary widely and signal multiple possible outcomes for Leidos’ future.

Explore 8 other fair value estimates on Leidos Holdings – why the stock might be worth as much as 60% more than the current price!

Build Your Own Leidos Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Ready To Venture Into Other Investment Styles?

Early movers are already taking notice. See the stocks they’re targeting before they’ve flown the coop:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

-

Business1 week ago

Business1 week agoThe Guardian view on Trump and the Fed: independence is no substitute for accountability | Editorial

-

Tools & Platforms4 weeks ago

Building Trust in Military AI Starts with Opening the Black Box – War on the Rocks

-

Ethics & Policy1 month ago

Ethics & Policy1 month agoSDAIA Supports Saudi Arabia’s Leadership in Shaping Global AI Ethics, Policy, and Research – وكالة الأنباء السعودية

-

Events & Conferences4 months ago

Events & Conferences4 months agoJourney to 1000 models: Scaling Instagram’s recommendation system

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoMumbai-based Perplexity Alternative Has 60k+ Users Without Funding

-

Education2 months ago

Education2 months agoVEX Robotics launches AI-powered classroom robotics system

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoHappy 4th of July! 🎆 Made with Veo 3 in Gemini

-

Funding & Business2 months ago

Funding & Business2 months agoKayak and Expedia race to build AI travel agents that turn social posts into itineraries

-

Education2 months ago

Education2 months agoMacron says UK and France have duty to tackle illegal migration ‘with humanity, solidarity and firmness’ – UK politics live | Politics

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoOpenAI 🤝 @teamganassi