Tools & Platforms

UBS Picks the Superior AI Stock to Buy After Earnings

The AI boom is nearly 3 years old, and one thing is certain about it: the boom has legs, and AI is here to stay. More and more companies are turning to the technology to enhance all sorts of functions, from customer service to chatbots to high-level data analytics and even to decision-making processes. According to Fortune Business Insights, up to 35% of all businesses have integrated AI into their work models.

-

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

This equals big money for the AI developers out there. Chip makers, AI app creators, data analysis firms – all of these and more have created an industry that was valued at $233 billion last year, and is estimated by Fortune Business Insights to hit $294 billion this year – and to show a CAGR of 29.2% through 2032, reaching $1.77 trillion that year. We should note that North American AI companies, mainly in the US, are leading this industry, with a 2024 market share of nearly 33%.

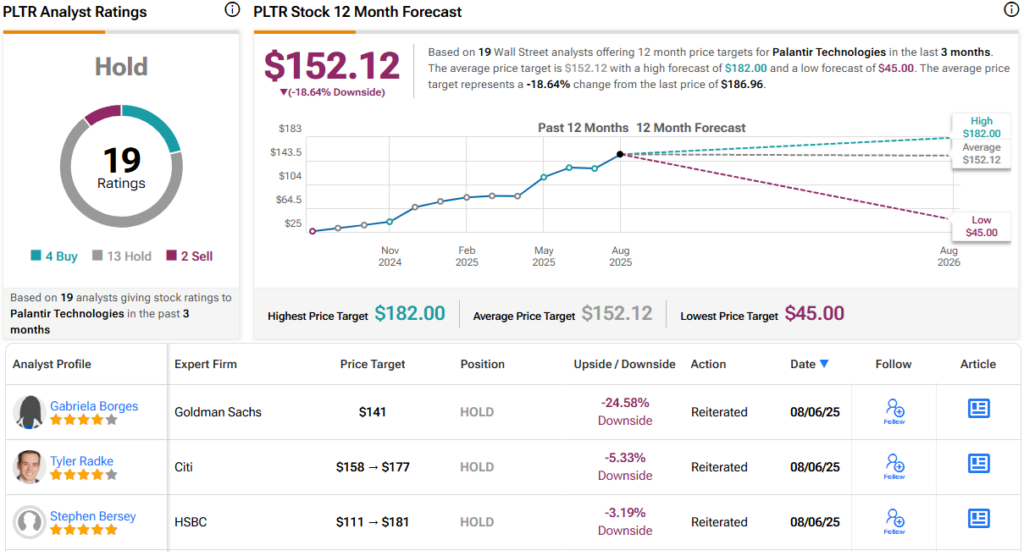

With numbers like these, it’s no surprise that UBS analysts are combing through the sector to pinpoint the most promising AI stocks. Their latest deep dive zeroes in on two recent earnings reporters – Palantir (NASDAQ:PLTR) and Advanced Micro Devices (NASDAQ:AMD) – to see which is the superior AI stock to buy. Let’s take a closer look.

Palantir

The first AI stock we’ll look at here is one of the leaders in the field. Palantir is well-known for marrying AI technology and capabilities to the field of data analysis, a match that has matured into a solid product platform – AIP, or AI Platform – and a set of tools whose wide applicability has made them highly popular. Since its founding in 2003, Palantir has developed a reputation for innovation, and has built itself into a $441 billion giant of the AI industry.

Palantir’s AIP is purpose-built to combine AI tech with human intuition and flexibility, to gain the best from both – and to improve outcomes and results in data analysis. The products also use AI technology to improve the user interface, making it easy to use and simple to understand. The AI reads and responds in real text, based on natural language models; in practice, Palantir’s users don’t need to learn machine language or computer coding to communicate with the AI – they can simply enter their requests in clear text and receive responses the same way. The technology is also amenable to real-time translations, making Palantir’s products easy to market internationally – the system just needs to be told what language it is using, and its translation algorithms handle the rest.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Infinities Technology International (Cayman) Holding Limited ( (HK:1961) ) has provided an announcement.

Infinities Technology International reported a significant decline in revenue and gross profit for the first half of 2025, with an 85.8% drop in revenue compared to the same period in 2024. This decline is attributed to reduced revenue from its mobile games and digital media businesses, as well as the early-stage development of its AI application services, which have yet to generate substantial profits. Despite these challenges, the company remains focused on its strategic goal of expanding its digital entertainment platform globally, leveraging AI as a core component. The industry outlook is optimistic, with the Chinese government’s recent AI initiative expected to drive significant development and investment opportunities in the sector.

The most recent analyst rating on (HK:1961) stock is a Hold with a HK$0.50 price target. To see the full list of analyst forecasts on Infinities Technology International (Cayman) Holding Limited stock, see the HK:1961 Stock Forecast page.

More about Infinities Technology International (Cayman) Holding Limited

Infinities Technology International (Cayman) Holding Limited operates in the digital entertainment industry, focusing on mobile games, digital media, and gaming product supply. The company is committed to building a diversified digital entertainment service platform with a strong emphasis on artificial intelligence technologies.

Average Trading Volume: 404,103

Technical Sentiment Signal: Sell

Current Market Cap: HK$198.3M

For detailed information about 1961 stock, go to TipRanks’ Stock Analysis page.

Brands caught using AI have continued to face backlash from consumers. Last month, Guess sparked outcry online when it featured an AI-generated model in an advertisement that appeared in Vogue.

So even outside of any obvious mistakes made by AI tools, some artists say their clients simply want a human touch to distinguish themselves from the growing pool of AI-generated content online.

To Todd Van Linda, an illustrator and comic artist in Florida, AI art is easily discernible, if not by certain telltale inconsistencies in the details, then by the plasticine effect that defines AI-generated images across a range of styles.

“I can look at a piece and not only tell that it’s AI, I can tell you what descriptor they used to generate it,” Van Linda said. “When it comes to, especially, independent authors, they don’t want anything to do with that because it’s so formulaic, it’s obvious. It’s like they stopped off at Walmart to get a bargain cover for their book.”

Authors come to him, he said, because they know that AI-generated art fails to capture the hyperspecific “vibe” of their individual story. Often, his clients can only give him a rough idea of what they want. It’s then Van Linda’s job to decipher their preferences and create something that draws out the exact feeling each client seeks to evoke from their art.

Van Linda said he also gets approached by people who want him to “fix” their AI-generated art, but he avoids those jobs now because he has realized those clients are typically less willing to pay him what he believes his labor is worth.

“There would be more work involved in fixing those images than there would be in starting from a clean sheet of paper and doing it right, because what they have is a mismatched collection of generalities that really don’t follow what they’re trying to do,” he said. “But they’re trying to wedge the square peg into the round hole because they don’t want to spend any more money.”

The low pay from clients who have already cheaped out on AI tools has affected gig workers across industries, including more technical ones like coding. For India-based web and app developer Harsh Kumar, many of his clients say they had already invested much of their budget in “vibe coding” tools that couldn’t deliver the results they wanted.

But others, he said, are realizing that shelling out for a human developer is worth the headaches saved from trying to get an AI assistant to fix its own “crappy code.” Kumar said his clients often bring him vibe-coded websites or apps that resulted in unstable or wholly unusable systems.

His projects have included fixing an AI-powered support chatbot that gave customers inaccurate answers — and sometimes leaked sensitive system details due to poor safety measures — and rebuilding an AI content recommendation system that frequently crashed, gave irrelevant recommendations and exposed sensitive data.

“AI may increase productivity, but it can’t fully replace humans,” Kumar said. “I’m still confident that humans will be required for long-term projects. At the end of the day, humans were the ones who developed AI.”

Tools & Platforms

How New Cloud and AI Security Partnerships at Akamai Technologies (AKAM) Have Changed Its Investment Story

- On August 13, 2025, Aptum announced a new partnership with Akamai Technologies to deliver cloud migration and transformation services, while Akamai also revealed a collaboration with Aqua Security to bolster AI-powered cloud security for enterprise customers.

- These recent deals signal Akamai’s growing efforts to accelerate innovation in cloud and AI security, aligning its platform with evolving enterprise technology priorities.

- We’ll examine how Akamai’s expanded cloud services partnerships may influence its investment narrative and future growth outlook.

Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Akamai Technologies Investment Narrative Recap

To be comfortable owning Akamai Technologies, investors must believe the company can offset secular declines in its legacy delivery business by scaling its cloud, compute, and security offerings quickly enough to drive sustained revenue and profit growth. The recent partnerships with Aptum and Aqua Security underscore Akamai’s intent to align its platform with rising AI and security demands, but they do not yet materially alter the short-term catalyst of accelerating cloud revenue or reduce the main risk of margin pressure from capital-intense expansion.

Among the latest developments, Akamai’s August 13 announcement with Aptum stands out, as it connects directly to the ongoing catalyst of expanding Cloud Infrastructure Services (CIS) revenue. By partnering to offer integrated cloud migration services, Akamai aims to deepen enterprise adoption of its cloud platform, which is essential for driving the top-line growth expected as part of its transformation story.

Yet, investors should not overlook that increasing capital expenditures to support these new cloud and AI initiatives could pressure net margins if scaling proves slower or costlier than anticipated…

Read the full narrative on Akamai Technologies (it’s free!)

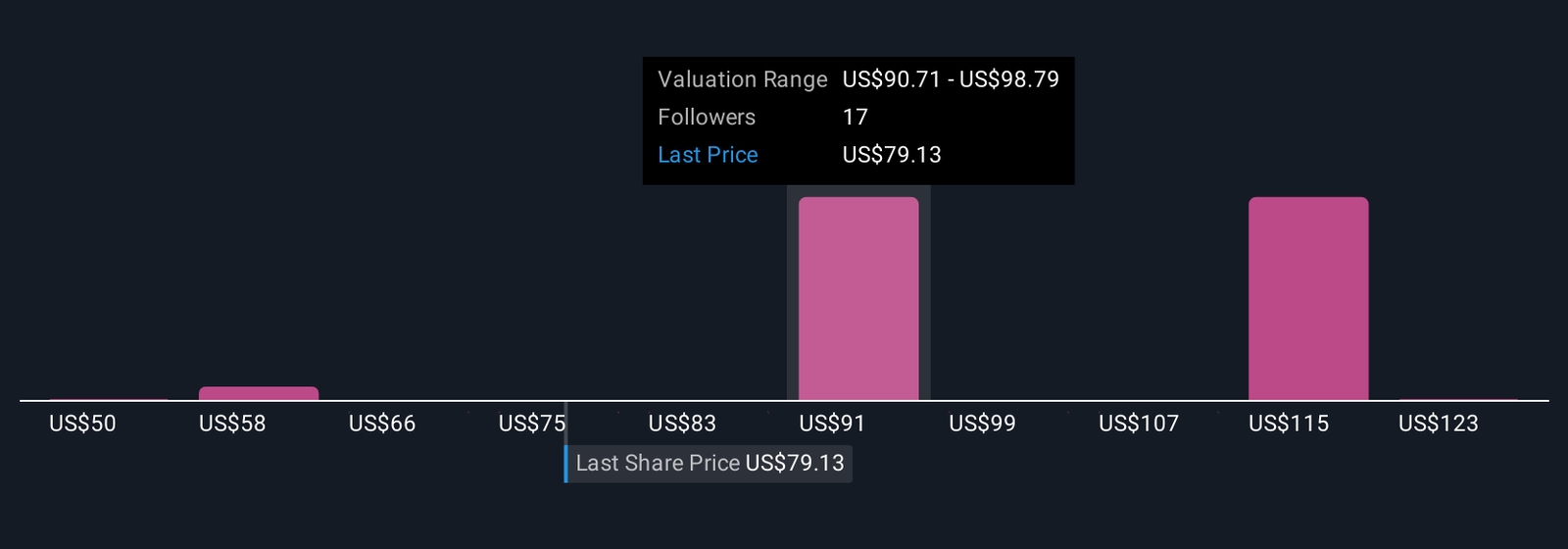

Akamai Technologies’ narrative projects $4.9 billion in revenue and $765.1 million in earnings by 2028. This requires 6.1% yearly revenue growth and a $340.5 million earnings increase from $424.6 million currently.

Uncover how Akamai Technologies’ forecasts yield a $95.20 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Six members of the Simply Wall St Community estimate Akamai’s fair value between US$50.32 and US$131.10 per share. While bullish cloud catalysts are top of mind, many investors continue to weigh margin and profitability risks before setting expectations for the company’s path forward.

Explore 6 other fair value estimates on Akamai Technologies – why the stock might be worth as much as 66% more than the current price!

Build Your Own Akamai Technologies Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Contemplating Other Strategies?

Don’t miss your shot at the next 10-bagger. Our latest stock picks just dropped:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

-

Tools & Platforms3 weeks ago

Building Trust in Military AI Starts with Opening the Black Box – War on the Rocks

-

Ethics & Policy1 month ago

Ethics & Policy1 month agoSDAIA Supports Saudi Arabia’s Leadership in Shaping Global AI Ethics, Policy, and Research – وكالة الأنباء السعودية

-

Business2 days ago

Business2 days agoThe Guardian view on Trump and the Fed: independence is no substitute for accountability | Editorial

-

Events & Conferences3 months ago

Events & Conferences3 months agoJourney to 1000 models: Scaling Instagram’s recommendation system

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoMumbai-based Perplexity Alternative Has 60k+ Users Without Funding

-

Funding & Business2 months ago

Funding & Business2 months agoKayak and Expedia race to build AI travel agents that turn social posts into itineraries

-

Education2 months ago

Education2 months agoVEX Robotics launches AI-powered classroom robotics system

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoHappy 4th of July! 🎆 Made with Veo 3 in Gemini

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoOpenAI 🤝 @teamganassi

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoAstrophel Aerospace Raises ₹6.84 Crore to Build Reusable Launch Vehicle