AI Research

AI Data Centers Market Size to Hit USD 165.73 Billion by 2034

AI Data Centers Market Size and Forecast 2025 to 2034

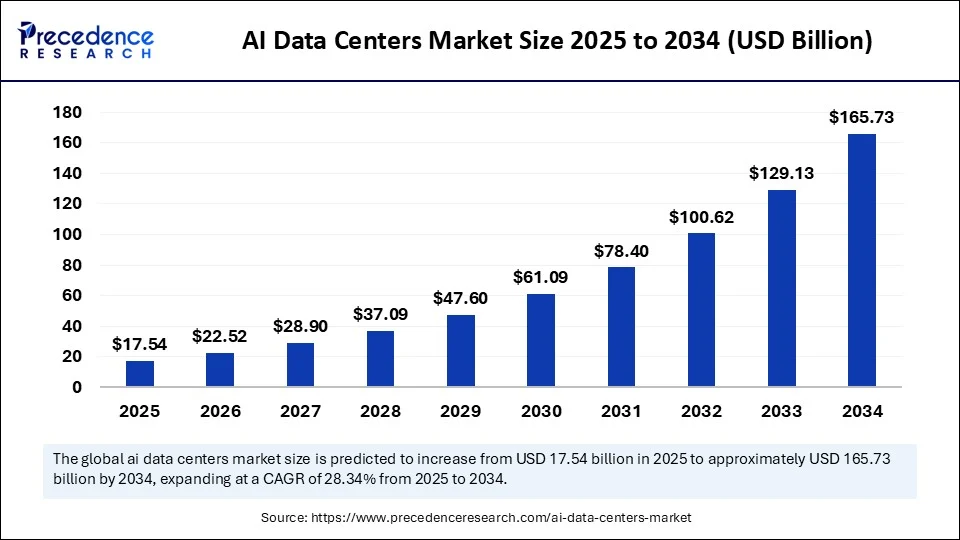

The global AI data centers market size was calculated at USD 13.67 billion in 2024 and is predicted to increase from USD 17.54 billion in 2025 to approximately USD 165.73 billion by 2034, expanding at a CAGR of 28.34% from 2025 to 2034. The rising adoption of AI technologies to streamline data transmission drives the growth of the AI data centers market. The demand for high-performance computing power has increased, further contributing to market growth.

AI Data Centers Market Key Takeaways

- In terms of revenue, the global AI data centers market was valued at USD 13.67 billion in 2024.

- It is projected to reach USD 165.73 billion by 2034.

- The market is expected to grow at a CAGR of 28.34% from 2025 to 2034.

- North America dominated the AI data centers market with the largest share of 39% in 2024.

- Asia Pacific is expected to grow at a significant CAGR from 2025 to 2034.

- By component, the hardware segment contributed the biggest market share of 58% in 2024.

- By component, the services segment will expand at a significant CAGR between 2025 and 2034.

- By data center type, the hyperscale AI data centers segment captured the highest market share of 64% in 2024.

- By data center type, the edge AI data centers segment will grow at a notable CAGR between 2025 and 2034.

- By AI workload type, the training workloads segment held the largest market share of 45% in 2024.

- By AI workload type, the generative AI segment will expand at a significant CAGR between 2025 and 2034.

- By cooling infrastructure, the air cooling segment contributed the biggest market share of 62% in 2024.

- By cooling infrastructure, the liquid cooling segment will expand at a significant CAGR between 2025 and 2034.

- By power capacity, the 20–50 MW segment led the market generated the major market share of 36% in 2024.

- By power capacity, the above 50 MW segment will grow at a CAGR between 2025 and 2034.

- By deployment mode, the cloud-based segment accounted for a significant market share of 52% in 2024.

- By deployment mode, the hybrid cloud segment will expand to a remarkable CAGR between 2025 and 2034.

- By end-user industry, the technology & cloud providers segment held the major market share of 48% in 2024.

- By end-user industry, the healthcare & life sciences segment will expand at a significant CAGR between 2025 and 2034.

U.S. AI Data Centers Market Size and Growth 2025 to 2034

The U.S. AI data centers market size was evaluated at USD 3.73 billion in 2024 and is projected to be worth around USD 46.15 billion by 2034, growing at a CAGR of 28.60% from 2025 to 2034.

What Made North America the Dominant Region in the AI Data Centers Market in 2024?

North America dominated the AI data centers market with a major revenue share in 2024 due to its robust, technologically advanced infrastructure, strong investors in AI-ready data center infrastructures, and rapid AI adoption in various industries, aligning with government support and initiatives. The rising demand for AI technologies across various industries and the growing focus on green AI data centers are boosting the regional market growth. Additionally, the strong existence of key market players like Microsoft. IBM and NVIDIA are driving innovative approaches in AI data centers.

The U.S. is a major player in the regional market. The U.S. has an advanced technological infrastructure with the presence of key market player and their investments in AI capabilities. The U.S.-based companies are increasing their AI-ready data center infrastructure investments to support emerging technologies like big data analytics, machine learning, and generative AI. The rapid adoption of AI across the country is fostering market growth.

- In July 2025, the U.S. Department of Energy (DOE) announced a new step on the Donald Trump administration’s plan for accelerating the development of AI infrastructure by siting on DOE lands. The DOE has selected its four sites, such as Idaho National Laboratory, Oak Ridge Reservation, Paducah Gaseous Diffusion Plant, and Savannah River Site, while inviting private sector partners for the development of advanced AI data centers and energy generation projects. (Source: https://www.energy.gov)

")

Asia Pacific AI Data Centers Market Trends

Asia Pacific is expected to grow at the fastest rate in the coming years, driven by the increasing adoption of AI services and adoption of cutting-edge computer infrastructure. The government of Asia is implementing several regulations and policies to promote the use of digital technologies and cloud services. The government-led AI initiatives are boosting the adoption of AI-enabled analytics and edge technologies. Additionally, the smart city projects are further contributing to the need for robust AI-ready data centers in Asia. Cities like Singapore, Tokyo, and Sydney are the major hubs for AI-driven data centers in Asia.

China is a major player in the regional market, contributing to growth due to the expanding digital economy and government investments in AI infrastructure. The government initiatives in promoting AI adoption, developments, and data center constructions are fostering this growth. Additionally, country investments in innovations, including underwater cooling technology for data centers, further add to market growth.

India is a significant player in the regional market. This is mainly due to rapid AI adoption, expanding IT infrastructures, and government promotion for digitalization across various industries. The Government of India is investing heavily in advancing data center infrastructure, leveraging AI in its practices, and fueling the market.

- The cutting-edge data centers in India, including Yotta NM1, Reliance Jio’s AI data centers, AdaniConneX data centers, CtrlS AI Mega Campus, and ST Telemedia Global Data Centers (STT GDC India), are driving significant innovations and investments in data center infrastructure.

Europe AI Data Centers Market Trends

Europe is expected to grow at a notable rate during the projection period due to rapid digitalization and demand for IoT technologies in the region. The adoption of cloud computing has increased. Europe is a hub for sustainable initiatives, emphasizes renewable energy sources and energy designs, and has a significant focus on AI data centers. The hyperscalers are taking the largest portion of data center capacity in Europe, which is expected to bring out significant and novel data center capabilities by 2025.

Countries like the UK, Germany, and France are leading the regional market, driven by the UK’s national AI strategy, Germany’s larger data center abilities, the digital transformation and sustainability, and France’s AI for Humanity strategies.

- In January 2025, the European government released its AI Opportunities Action Plan, which includes a large number of policies and actions for the government to take part in its overarching aspiration to enhance economic growth.

- In February 2025, France invests €109 billion in its AI sector, with a €30 billion and a €50 billion commitment from the UAE to finance a 1-gigawatt data center, which is four times the power capacity of the UK’s largest operational facility. (Source: https://www.pillsburylaw.com)

Market Overview

AI data centers are specialized computing facilities designed and optimized to handle the massive data processing and compute-intensive workloads associated with Artificial Intelligence (AI) and Machine Learning (ML) applications. Unlike traditional data centers, AI data centers integrate high-performance hardware (e.g., GPUs, TPUs), advanced cooling systems, and AI-specific infrastructure software to train and infer AI models at scale. They support workloads like generative AI, deep learning, NLP, computer vision, and real-time analytics. Companies are investing heavily in hardware like AI-optimized chips and services, leading to improved data center performance. The rising need for cutting-edge data centers in industries like BFSI is fueling the market expansion.

What are the Key Trends in the AI Data Centers Market?

- Expanding Cloud Computing: The expanding cloud computing is driving the need for cutting-edge data center infrastructure with AI integration.

- Demand for High-Performance Computing Power: The demand for high-performance computing power has increased to handle complex AI models and large datasets, driving innovations in AI data centers.

- Adoption of AI Applications: AI applications have increased in industries like data analytics, machine learning, and generative AI, driving the need for strong data center infrastructures.

- Technological Advancements: Advancements in technologies like 5G networks, AI-driven analytics, and IoT devices prompt the urgent need for robust data center infrastructure.

- Sustainability Concerns: The growing emphasis on building data centers with less environmental impact, the implementation of energy-efficient cooling systems, the use of renewable energy sources, and the utilization of eco-friendly materials in construction are driving focus on AI data centers.

Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 165.73 Billion |

| Market Size in 2025 | USD 17.54 Billion |

| Market Size in 2024 | USD 13.67 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 28.34% |

| Dominating Region | Asia Pacific |

| Fastest Growing Region | North America |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Component, Data Center Type, AI Workload Type, Cooling Infrastructure, Power Capacity, Deployment Mode, End-User Industry, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Market Dynamics

Drivers

Digital Transformation

The rapid digital transformation is boosting the need for AI-driven data centers globally. The demand for AI-powered applications has increased. Data centers support these demanding applications, including infrastructures for deep learning, generative AI, and machine learning. The growth of cloud computing is driving the need for AI data centers, driven by the requirement for scalable and flexible cloud services. Additionally, the growing adoption of edge computing and low-latency processing contributes to digital transformation accelerations. The government initiatives in promoting the use of digital technologies in various industries like healthcare, banking, automotives, and others, with growing emphasis on sustainability and energy efficiency, are fostering this transformation. These promotions are mitigating high-energy consumption and reducing greenhouse gas emissions, making a significant step toward AI-powered data centers.

Restraint

Concerns Over Data Privacy and Cybersecurity

Data privacy and cybersecurity concerns are the major challenges for the global AI data centers market. Data centers have a high risk of data breaches, making them challenging ecosystems for regulatory damage, regulatory analyses, and overall financial loss. AI data centers are vulnerable to cybersecurity attacks, like ransomware attacks, hacking, and malware, which hampers data integrity and availability. The Government has implemented several strict data protection regulations, including GDPR and CCPA, making it essential for AI data centers to implement security measures, which leads to increased cost and complexity. AI data centers can mitigate such barriers by implementing strong security measures, conducting regular security audits, and investing in cybersecurity talents.

Opportunity

Government Investments and Regulations

Government initiatives in promoting the use of digital technologies and investments in digital infrastructure, like data centers, are fostering innovations and advancements in AI-driven data centers. Governments worldwide have implemented several regulations for data protection and privacy, such as the General Data Protection Regulation (GDPR), which contributes to the increasing need for secure data storage solutions. Government funding for AI research and development, and support for adoption of cloud computing and data centers policies, are bringing significant opportunities for the AI data centers. Additionally, green initiatives and support for sustainability plans are further leveraging initiatives in AI data center infrastructure.

- On July 23, 2025, President Donald Trump signed three AI-related Executive Orders for implementing the recently released White House’s Artificial Intelligence (AI) Action Plan. (Source: https://www.workforcebulletin.com)

Component Insights

Which Component Segment Dominate the AI Data Centers Market in 2024?

The hardware segment dominated the market with the largest share in 2024. This is mainly due to its ability to enhance the performance and power efficiency of AI workloads. Hardware is playing a crucial role in enhancing sustainability and energy efficiency in data centers. The demand for specialized hardware like GPUs and ASICs has increased for AI computer capacity. Additionally, the growing adoption of liquid cooling and advancements in chip designs are driving the importance of hardware to enhance the efficiency and power of AI data centers.

The services segment is expected to grow at the fastest rate during the projection period, driven by increased AI deployment complexity and the requirement for expert supporting services in infrastructure management. The adoption of hybrid and multi-cloud ecosystems has increased, driving demand for services to handle both on-premises and cloud-based systems. Services like consulting, implementation, integration, managed, and maintenance services are highly in demand.

Data Center Type Insights

What Made Hyperscale AI Data Centers the Dominant Segment in the AI Data Centers Market in 2024?

The hyperscale AI data centers segment dominated the market in 2024. This is mainly due to their ability to offer scalable, flexible, high computing power, and networking required for meeting growing demands. The hyperscale AI data centers can handle large-scale AI workloads. The advanced architecture of hyperscale AI data centers helps to support high-density services and AI accelerators, including TPUs and GPUs.

The edge AI data centers segment is expected to expand a the fastest CAGR over the forecast period, due to increased demand for real-time data processing and low-latency applications. The edge AI data centers enable quick decision making through their real-time data processing and reduce bandwidth constraints. The increasing adoption of IoT devices and 5G networking has increased the need for AI decentralization in industries like smart manufacturing, healthcare, and automotives to reduce latency and process data closer to the source.

AI Workload Type Insights

Why Did the Training Workloads Segment Dominate the AI Data Centers Market in 2024?

The training workloads segment dominated the market in 2024 due to high computational requirements and specialized facilities. The training workloads are crucial in high-performance computing. The increased adoption of AI and ML into applications ike pattern recognition, data analysis, and predictive modelling is driving the need for training workloads.

The generative AI segment is expected to expand at the highest CAGR in the upcoming period, driven by the increased demand for strong infrastructure to support large amounts of data processing and complex computations. Generative AI streamlines the data centers’ workflow. The expanding generative AI movements have contributed to increased demand for data center GPUs, CPUs, DPU, AI ASICs, and networking ASICs.

Cooling Infrastructure Insights

Which Cooling Infrastructure Segment Dominate the AI Data Centers Market in 2024?

The air cooling segment dominated the market with the largest share in 2024, due to its ability to maintain an optimal temperature level. The expanding data centers drive the need for efficient cooling solutions like air cooling. Air-cooling solutions like room-based cooling and air handling units are essential in maintaining optimal airflow, temperature, and humidity levels. Ongoing advancements in air cooling, like enhanced efficiency and reduced energy consumption, further contribute to the segment’s growth.

The liquid cooling segment is likely to grow at the fastest CAGR in the upcoming period. The growth of the segment is driven by increased demand for energy-efficient cooling solutions. High-performance computing and AI-related workloads require liquid cooling solutions. The Direct-to-Chip Liquid Cooling sub-segment is leading the charge, driven by increased demand for thermal efficiency in high computational environments.

Power Capacity Insights

What Made 20-50 MW the Dominant Segment in the AI Data Centers Market in 2024?

The 20–50 MW segment dominated the market in 2024, due to its wide use in enterprises running AI workloads along with traditional applications. The small to medium data centers typically range between 20–50 MW. The 20–50 MW segment power capacity enables a balance between power capacity and scalability.

The above 50 MW segment is expected to grow at the fastest rate over the forecast period, driven by its utilization in large-scale facilities with higher power capacity demands. The AI data centers with above 50 MW power capacity offer hyperscale applications, high-performance computing, and support large AI workloads. The increased use of digital technologies has driven the need for large-scale AI data centers with more than 50 MW power capacity.

Deployment Mode Insights

How Does the Cloud-Based Segment Leads the AI Data Centers Market?

The cloud-based segment led the market in 2024 due to increased adoption of AI and cloud computing. The cloud-based AI data centers are flexible, scalable, cost-effective, and speed to setup. These data centers offer pre-configured AI tools, helping to reduce costs and enhance efficiency. The growing popularity of AI-as-a-service has contributed to the need for cloud-based AI data centers.

The hybrid cloud segment is likely to grow at the fastest rate in the coming years due to its scalability, flexibility, and affordability. The hybrid cloud-based data centers combine both on-premises and cloud infrastructures. The deployment of hybrid cloud has increased for more security & compliance, growing demand for edge computing, and AI integration for enabling cutting-edge data analysis and automations.

End-Use Industry Insights

Why Did the Technology & Cloud Service Providers Segment Dominate the AI Data Centers Market in 2024?

The technology & cloud service providers segment dominated the market in 2024, due to increased demand for cloud computing services. The technology giants and cloud service providers are becoming more visible due to increased adoption of cloud services and the need for data centers. Additionally, the adoption of multi-cloud strategies and hybrid strategies is driving the need for hybrid cloud management solutions, interconnection platforms, and services. The technology & cloud providers play a crucial role in increased AI and ML integration.

The healthcare & life sciences segment is expected to expand at the highest CAGR during the forecast period due to increased adoption of AI in the healthcare & life sciences industry. The utilization of AI for personalized medicine and genomics areas is contributing to the market growth. Personalized medicine and genomics require a large amount of data storage and analysis, driving demand for AI data centers. Additionally, the rapid digital transformation in the healthcare industry is fostering this growth.

AI Data Centers Market Companies

- NVIDIA Corporation

- AMD (Advanced Micro Devices)

- Intel Corporation

- Broadcom Inc.

- Micron Technology

- Marvell Technology

- Samsung Electronics

- SK hynix Inc.

- TSMC (Taiwan Semiconductor Manufacturing Company)

- Supermicro (Super Micro Computer, Inc.)

- Dell Technologies

- Hewlett-Packard Enterprise (HPE)

- Lenovo Group Ltd.

- Inspur Group

- Cisco Systems, Inc.

- Arista Networks

- Equinix, Inc. (data center infrastructure & interconnection)

- Vertiv Holdings Co. (power & cooling systems)

- Eaton Corporation

- Huawei Technologies Co., Ltd.

Recent Developments

- In July 2025, Google announced investments of $25 billion in data centers and artificial intelligence infrastructure, more than the next two years, in states across the biggest electric grid in the U.S. (Source: https://www.cnbc.com)

- In April 2025, Nvidia announced $500 billion for building AI infrastructure in the U.S. over the next four years, under the collaboration of TSM, the latest American tech firm backing the Trump administration’s push for local manufacturing giants.

(Source: https://cio.economictimes.indiatimes.com) - In January 2025, Microsoft announced investments of $80 billion in FY25 for the construction of data centers to handle artificial intelligence workloads. Over half of the expected AI infrastructure spending took place in the U.S.

(Source: https://www.cnbc.com) - In July 2025, a global leader in hyperscale digital infrastructure, Khazna Data Centers, partnered with Eni, a global integrated energy company, under a Heads of Terms (HOT) agreement set up as a joint venture for the development of an “AI Data Center Campus” with a total IT capacity of 500 MW in Ferrera Erbognone, Lombarly. (Source: https://www.eni.com)

- In April 2025, a leading AI-ready data center provider in India, ST Telemedia Global Data Centers, announced enhancing its data center landscape in Eastern India by launching its state-of-the-art facility in New Town, Kolkata. This next-generation campus is established on 5.59 acres and engineered to support the rising demands of AI computing with high-density rack configurations, cutting-edge cooling systems, and a modular and scalable design. (Source: https://www.sttelemediagdc.com)

Segment Covered in the Report

By Component

- Hardware

- Compute (GPUs, CPUs, TPUs, ASICs)

- Memory (HBM, DRAM, Flash)

- Storage (NVMe SSD, HDD, Object Storage)

- Networking (Switches, Routers, Interconnects)

- Software

- AI Workload Management Platforms

- Orchestration Tools (e.g., Kubernetes for AI)

- Virtualization & Containerization Software

- AI Model Training/Inference Frameworks

- Services

- Deployment & Integration

- Managed Services

- Consulting & Support

By Data Center Type

- Hyperscale AI Data Centers

- Colocation AI Data Centers

- Edge AI Data Centers

- Enterprise (Private) AI Data Centers

By AI Workload Type

- Training Workloads

- Inference Workloads

- Real-Time Analytics

- Generative AI

- Reinforcement Learning

By Cooling Infrastructure

- Liquid Cooling

- Immersion Cooling

- Direct-to-Chip Liquid Cooling

- Air Cooling

- CRAH/CRAC Units

- Chilled Water Systems

- Hybrid Cooling Systems

By Power Capacity

- Below 5 MW

- 5–20 MW

- 20–50 MW

- Above 50 MW

By Deployment Mode

- On-Premise

- Cloud-Based

- Hybrid Cloud

By End-User Industry

- Technology & Cloud Service Providers

- BFSI

- Healthcare & Life Sciences

- Automotive (Autonomous Driving)

- Retail & E-commerce

- Government & Defense

- Telecom

- Energy & Utilities

- Education & Research

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Conservative leader Kemi Badenoch has said her party will remove all net zero requirements on oil and gas companies drilling in the North Sea if elected.

Badenoch is to formally announce the plan to focus solely on “maximising extraction” and to get “all our oil and gas out of the North Sea” in a speech in Aberdeen on Tuesday.

Reform UK has said it wants more fossil fuels extracted from the North Sea.

The Labour government has committed to banning new exploration licences. A spokesperson said a “fair and orderly transition” away from oil and gas would “drive growth”.

Exploring new fields would “not take a penny off bills” or improve energy security and would “only accelerate the worsening climate crisis”, the government spokesperson warned.

Badenoch signalled a significant change in Conservative climate policy when she announced earlier this year that reaching net zero would be “impossible” by 2050.

Successive UK governments have pledged to reach the target by 2050 and it was written into law by Theresa May in 2019. It means the UK must cut carbon emissions until it removes as much as it produces, in line with the 2015 Paris Climate Agreement.

Now Badenoch has said that requirements to work towards net zero are a burden on oil and gas producers in the North Sea which are damaging the economy and which she would remove.

The Tory leader said a Conservative government would scrap the need to reduce emissions or to work on technologies such as carbon storage.

Badenoch said it was “absurd” the UK was leaving “vital resources untapped” while “neighbours like Norway extracted them from the same sea bed”.

In 2023, then Prime Minister Rishi Sunak granted 100 new licences to drill in the North Sea which he said at the time was “entirely consistent” with net zero commitments.

Reform UK has said it will abolish the push for net zero if elected.

The current government said it had made the “biggest ever investment in offshore wind and three first of a kind carbon capture and storage clusters”.

Carbon capture and storage facilities aim to prevent carbon dioxide (CO2) produced from industrial processes and power stations from being released into the atmosphere.

Most of the CO2 produced is captured, transported and then stored deep underground.

It is seen by the likes of the International Energy Agency and the Climate Change Committee as a key element in meeting targets to cut the greenhouse gases driving dangerous climate change.

Esme Stallard and Justin RowlattClimate and science team

Sean Gallup/Getty Images

Sean Gallup/Getty ImagesIt is smaller than your fingernail, but this hairy beetle is one of the biggest single threats to the UK’s forests.

The bark beetle has been the scourge of Europe, killing millions of spruce trees, yet the government thought it could halt its spread to the UK by checking imported wood products at ports.

But this was not their entry route of choice – they were being carried on winds straight over the English Channel.

Now, UK government scientists have been fighting back, with an unusual arsenal including sniffer dogs, drones and nuclear waste models.

They claim the UK has eradicated the beetle from at risk areas in the east and south east. But climate change could make the job even harder in the future.

The spruce bark beetle, or Ips typographus, has been munching its way through the conifer trees of Europe for decades, leaving behind a trail of destruction.

The beetles rear and feed their young under the bark of spruce trees in complex webs of interweaving tunnels called galleries.

When trees are infested with a few thousand beetles they can cope, using resin to flush the beetles out.

But for a stressed tree its natural defences are reduced and the beetles start to multiply.

“Their populations can build to a point where they can overcome the tree defences – there are millions, billions of beetles,” explained Dr Max Blake, head of tree health at the UK government-funded Forestry Research.

“There are so many the tree cannot deal with them, particularly when it is dry, they don’t have the resin pressure to flush the galleries.”

Since the beetle took hold in Norway over a decade ago it has been able to wipe out 100 million cubic metres of spruce, according to Rothamsted Research.

‘Public enemy number one’

As Sitka spruce is the main tree used for timber in the UK, Dr Blake and his colleagues watched developments on continental Europe with some serious concern.

“We have 725,000 hectares of spruce alone, if this beetle was allowed to get hold of that, the destructive potential means a vast amount of that is at risk,” said Andrea Deol at Forestry Research. “We valued it – and it’s a partial valuation at £2.9bn per year in Great Britain.”

There are more than 1,400 pests and diseases on the government’s plant health risk register, but Ips has been labelled “public enemy number one”.

The number of those diseases has been accelerating, according to Nick Phillips at charity The Woodland Trust.

“Predominantly, the reason for that is global trade, we’re importing wood products, trees for planting, which does sometimes bring ‘hitchhikers’ in terms of pests and disease,” he said.

Forestry Research had been working with border control for years to check such products for Ips, but in 2018 made a shocking discovery in a wood in Kent.

“We found a breeding population that had been there for a few years,” explained Ms Deol.

“Later we started to pick up larger volumes of beetles in [our] traps which seemed to suggest they were arriving by other means. All of the research we have done now has indicated they are being blown over from the continent on the wind,” she added.

Daegan Inward/Forestry Research

Daegan Inward/Forestry ResearchThe team knew they had to act quickly and has been deploying a mixture of techniques that wouldn’t look out of place in a military operation.

Drones are sent up to survey hundreds of hectares of forest, looking for signs of infestation from the sky – as the beetle takes hold, the upper canopy of the tree cannot be fed nutrients and water, and begins to die off.

But next is the painstaking work of entomologists going on foot to inspect the trees themselves.

“They are looking for a needle in a haystack, sometimes looking for single beetles – to get hold of the pioneer species before they are allowed to establish,” Andrea Deol said.

In a single year her team have inspected 4,500 hectares of spruce on the public estate – just shy of 7,000 football pitches.

Such physically-demanding work is difficult to sustain and the team has been looking for some assistance from the natural and tech world alike.

Tony Jolliffe/BBC

Tony Jolliffe/BBCWhen the pioneer Spruce bark beetles find a suitable host tree they release pheromones – chemical signals to attract fellow beetles and establish a colony.

But it is this strong smell, as well as the smell associated with their insect poo – frass – that makes them ideal to be found by sniffer dogs.

Early trials so far have been successful. The dogs are particularly useful for inspecting large timber stacks which can be difficult to inspect visually.

The team is also deploying cameras on their bug traps, which are now able to scan daily for the beetles and identify them in real time.

“We have [created] our own algorithm to identify the insects. We have taken about 20,000 images of Ips, other beetles and debris, which have been formally identified by entomologists, and fed it into the model,” said Dr Blake.

Some of the traps can be in difficult to access areas and previously had only been checked every week by entomologists working on the ground.

The result of this work means that the UK has been confirmed as the first country to have eradicated Ips Typographus in its controlled areas, deemed to be at risk from infestation, and which covers the south east and east England.

“What we are doing is having a positive impact and it is vital that we continue to maintain that effort, if we let our guard down we know we have got those incursion risks year on year,” said Ms Deol.

Tony Jolliffe/BBC

Tony Jolliffe/BBCAnd those risks are rising. Europe has seen populations of Ips increase as they take advantage of trees stressed by the changing climate.

Europe is experiencing more extreme rainfall in winter and milder temperatures meaning there is less freezing, leaving the trees in waterlogged conditions.

This coupled with drier summers leaves them stressed and susceptible to falling in stormy weather, and this is when Ips can take hold.

With larger populations in Europe the risk of Ips colonies being carried to the UK goes up.

The team at Forestry Research has been working hard to accurately predict when these incursions may occur.

“We have been doing modelling with colleagues at the University of Cambridge and the Met Office which have adapted a nuclear atmospheric dispersion model to Ips,” explained Dr Blake. “So, [the model] was originally used to look at nuclear fallout and where the winds take it, instead we are using the model to look at how far Ips goes.”

Nick Phillips at The Woodland Trust is strongly supportive of the government’s work but worries about the loss of ancient woodland – the oldest and most biologically-rich areas of forest.

Commercial spruce have long been planted next to such woods, and every time a tree hosting spruce beetle is found, it and neighbouring, sometimes ancient trees, have to be removed.

“We really want the government to maintain as much of the trees as they can, particularly the ones that aren’t affected, and then also when the trees are removed, supporting landowners to take steps to restore what’s there,” he said. “So that they’re given grants, for example, to be able to recover the woodland sites.”

The government has increased funding for woodlands in recent years but this has been focused on planting new trees.

“If we only have funding and support for the first few years of a tree’s life, but not for those woodlands that are 100 or century years old, then we’re not going to be able to deliver nature recovery and capture carbon,” he said.

Additional reporting Miho Tanaka

-

Tools & Platforms3 weeks ago

Building Trust in Military AI Starts with Opening the Black Box – War on the Rocks

-

Ethics & Policy1 month ago

Ethics & Policy1 month agoSDAIA Supports Saudi Arabia’s Leadership in Shaping Global AI Ethics, Policy, and Research – وكالة الأنباء السعودية

-

Events & Conferences3 months ago

Events & Conferences3 months agoJourney to 1000 models: Scaling Instagram’s recommendation system

-

Business2 days ago

Business2 days agoThe Guardian view on Trump and the Fed: independence is no substitute for accountability | Editorial

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoMumbai-based Perplexity Alternative Has 60k+ Users Without Funding

-

Funding & Business2 months ago

Funding & Business2 months agoKayak and Expedia race to build AI travel agents that turn social posts into itineraries

-

Education2 months ago

Education2 months agoVEX Robotics launches AI-powered classroom robotics system

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoHappy 4th of July! 🎆 Made with Veo 3 in Gemini

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoOpenAI 🤝 @teamganassi

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoAstrophel Aerospace Raises ₹6.84 Crore to Build Reusable Launch Vehicle