AI Insights

1 Unstoppable Artificial Intelligence (AI) Growth Stock to Buy Before It Is Too Late

Jabil (JBL) may not be a household name for investors looking to capitalize on the rapid adoption of artificial intelligence (AI), but a closer look at the company’s recent results will make it clear that it is benefiting big-time from this technology.

Jabil is a contract electronics manufacturer that serves multiple industries, ranging from automotive to semiconductor equipment to networking to data centers. The company is now witnessing a nice acceleration in growth thanks to the fast-growing deployment of AI data center hardware, which is leading to an increase in demand for the company’s cloud data center-focused offerings such as rack integration services.

This explains why Jabil delivered solid quarterly results recently and also raised its full-year guidance. Let’s take a closer look at the company’s numbers and see why it would be a good idea to buy this stock right now.

Image source: Getty Images.

Jabil stock has received a nice AI-powered boost

Jabil released its fiscal 2025 third-quarter results (for the three months ended May 31) on June 17. The company’s revenue increased by 16% from the year-ago period, while earnings shot up 35% year over year. Even better, Jabil has raised its full-year revenue forecast to $29 billion from the prior estimate of $27.9 billion.

It now expects fiscal 2025 earnings to land at $9.33 per share from the earlier expectation of $8.95 per share. Jabil management remarked on the latest earnings conference call that it is witnessing an increase in demand for “complex server and rack integration, advanced networking, innovative power, and cooling solutions” on account of the growing deployment of AI data centers.

CEO Mike Dastoor said AI infrastructure demand is accelerating. The company estimates its AI revenue is on track to jump by 50% this year to $8.5 billion. AI, therefore, is set to account for almost 30% of Jabil’s top line in fiscal 2025. Not surprisingly, the company plans to invest $500 million in shoring up its cloud and AI data center infrastructure manufacturing services in the long run.

Jabil intends to spend this money on bolstering its ability to design and manufacture complex AI server racks that can meet the growing power requirements and liquid-cooling needs in data centers. Importantly, the AI server market is expected to grow at an annual pace of 34% through 2030, so it won’t be surprising to see AI moving the needle in a bigger way for the company.

What’s more, Jabil points out that its annual capex won’t increase because of the $500 million investment that it is planning, which should lead to an improvement in the company’s profitability going forward. Not surprisingly, Jabil’s earnings estimates have received a nice boost for the current and the next couple of fiscal years.

JBL EPS Estimates for Current Fiscal Year data by YCharts

Investors can still expect solid gains from this AI stock

Jabil stock has clocked respectable gains of 45% so far in 2025. That’s well above the 1% increase in the tech-laden Nasdaq Composite index this year. The important thing to note is Jabil isn’t all that expensive despite its recent surge. The stock has a forward price-to-earnings ratio of less than 20. That’s a discount to the Nasdaq-100 index’s average forward earnings multiple of 29 (using the index as a proxy for tech stocks).

Jabil’s bottom-line growth is set to accelerate over the next couple of years. So, it won’t be surprising to see this AI stock trading at a richer valuation in the future because of the improvement in its growth profile. Even if Jabil trades at 25 times earnings after a couple of years and achieves the $12.57 per share earnings that consensus estimates are projecting, its stock price could hit $314.

That would be a 50% jump from its current stock price. However, don’t be surprised to see the stock doing better than that as it has the potential to deliver stronger growth, which could lead the market to reward it with a higher multiple. All this makes Jabil a top growth stock to buy right now.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

AI Insights

91% of Jensen Huang’s $4.3 Billion Stock Portfolio at Nvidia Is Invested in Just 1 Artificial Intelligence (AI) Infrastructure Stock

Key Points

-

Most stocks that Nvidia and CEO Jensen Huang invest in tend to be strategic partners or companies that can expand the AI ecosystem.

-

For the AI sector to thrive, there is going to need to be a lot of supporting data centers and other AI infrastructure.

-

One stock that Nvidia is heavily invested in also happens to be one of its customers, a first-mover in the AI-as-a-service space.

-

10 stocks we like better than CoreWeave ›

Nvidia (NASDAQ: NVDA), the largest company in the world by market cap, is widely known as the artificial intelligence (AI) chip king and the main pick-and-shovel play powering the AI revolution. But as such a big company that is making so much money, the company has all sorts of different operations and divisions aside from its main business.

For instance, Nvidia, which is run by CEO Jensen Huang, actually invests its own capital in publicly traded stocks, most of which seem to have to do with the company itself or the broader AI ecosystem. At the end of the second quarter, Nvidia owned six stocks collectively valued at about $4.3 billion. However, of this amount, 91% of Nvidia’s portfolio is invested in just one AI infrastructure stock.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

A unique relationship

Nvidia has long had a relationship with AI data center company CoreWeave (NASDAQ: CRWV), having been a key supplier of hardware that drives the company’s business. CoreWeave builds data centers specifically tailored to meet the needs of companies looking to run AI applications.

Image source: Getty Images.

These data centers are also equipped with hardware from Nvidia, including the company’s latest graphics processing units (GPUs), which help to train large language models. Clients can essentially rent the necessary hardware to run AI applications from CoreWeave, which saves them the trouble of having to build out and run their own infrastructure. CoreWeave’s largest customer by far is Microsoft, which makes up roughly 60% of the company’s revenue, but CoreWeave has also forged long-term deals with OpenAI and IBM.

Nvidia and CoreWeave’s partnership dates back to at least 2020 or 2021, and Nvidia also invested in the company’s initial public offering earlier this year. Wall Street analysts say it’s unusual to see a large supplier participate in a customer’s IPO. But Nvidia may see it as a key way to bolster the AI sector because meeting future AI demand will require a lot of energy and infrastructure.

CoreWeave is certainly seeing demand. On the company’s second-quarter earnings call, management said its contract backlog has grown to over $30 billion and includes previously discussed contracts with OpenAI, as well as other new potential deals with a range of different clients from start-ups to larger companies. Customers have also been increasing the length of their contracts with CoreWeave.

“In short, AI applications are beginning to permeate all areas of the economy, both through start-ups and enterprise, and demand for our cloud AI services is aggressively growing. Our cloud portfolio is critical to CoreWeave’s ability to meet this growing demand,” CoreWeave’s CEO Michael Intrator said on the company’s earnings call.

Is CoreWeave a buy?

Due to the demand CoreWeave is seeing from the market, the company has been aggressively expanding its data centers to increase its total capacity. To do this, CoreWeave has taken on significant debt, which the capital markets seem more than willing to fund.

At the end of the second quarter, current debt (due within 12 months) grew to about $3.6 billion, up about $1.2 billion year over year. Long-term debt had grown to about $7.4 billion, up roughly $2 billion year over year. That has hit the income statement hard, with interest expense through the first six months of 2025 up to over $530 million, up from roughly $107 million during the same period in 2024.

CoreWeave reported a loss of $1.73 per share in the first six months of the year, better than the $2.23 loss reported during the same time period. Still, investors have expressed concern about growing competition in the AI-as-a-service space. They also question whether or not CoreWeave has a real moat, considering its customers and suppliers. For instance, while CoreWeave has a strong partnership with Nvidia, that does not prevent others in the space from forging partnerships. Additionally, CoreWeave’s main customers, like Microsoft, could choose to build their own data centers and infrastructure in-house.

CoreWeave also trades at over a $47 billion market cap but is still losing significant money. The valuation also means the company is trading at 10 times forward sales. Now, in fairness, CoreWeave has grown revenue through the first half of the year by 276% year over year. It all boils down to whether the company can maintain its first-mover advantage and whether the AI addressable market can keep growing like it has been.

I think investors can buy the stock for the more speculative part of their portfolio. The high dependence on industry growth and reliance on debt prevent me from recommending a large position at this time.

Should you invest $1,000 in CoreWeave right now?

Before you buy stock in CoreWeave, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CoreWeave wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $678,148!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,052,193!*

Now, it’s worth noting Stock Advisor’s total average return is 1,065% — a market-crushing outperformance compared to 186% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

See the 10 stocks »

*Stock Advisor returns as of August 25, 2025

Bram Berkowitz has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends International Business Machines, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Disclaimer: For information purposes only. Past performance is not indicative of future results.

Anthropic has agreed to pay $1.5 billion to settle a lawsuit brought by authors and publishers over its use of millions of copyrighted books to train the models for its AI chatbot Claude, according to a legal filing posted online.

A federal judge found in June that Anthropic’s use of 7 million pirated books was protected under fair use but that holding the digital works in a “central library” violated copyright law. The judge ruled that executives at the company knew they were downloading pirated works, and a trial was scheduled for December.

The settlement, which was presented to a federal judge on Friday, still needs final approval but would pay $3,000 per book to hundreds of thousands of authors, according to the New York Times. The $1.5 billion settlement would be the largest payout in the history of U.S. copyright law, though the amount paid per work has often been higher. For example, in 2012, a woman in Minnesota paid about $9,000 per song downloaded, a figure brought down after she was initially ordered to pay over $60,000 per song.

In a statement to Gizmodo on Friday, Anthropic touted the earlier ruling from June that it was engaging in fair use by training models with millions of books.

“In June, the District Court issued a landmark ruling on AI development and copyright law, finding that Anthropic’s approach to training AI models constitutes fair use,” Aparna Sridhar, deputy general counsel at Anthropic, said in a statement by email.

“Today’s settlement, if approved, will resolve the plaintiffs’ remaining legacy claims. We remain committed to developing safe AI systems that help people and organizations extend their capabilities, advance scientific discovery, and solve complex problems,” Sridhar continued.

According to the legal filing, Anthropic says the payments will go out in four tranches tied to court-approved milestones. The first payment would be $300 million within five days after the court’s preliminary approval of the settlement, and another $300 million within five days of the final approval order. Then $450 million would be due, with interest, within 12 months of the preliminary order. And finally $450 million within the year after that.

Anthropic, which was recently valued at $183 billion, is still facing lawsuits from companies like Reddit, which struck a deal in early 2024 to let Google train its AI models on the platform’s content. And authors still have active lawsuits against the other big tech firms like OpenAI, Microsoft, and Meta.

The ruling from June explained that Anthropic’s training of AI models with copyrighted books would be considered fair use under U.S. copyright law because theoretically someone could read “all the modern-day classics” and emulate them, which would be protected:

…not reproduced to the public a given work’s creative elements, nor even one author’s identifiable expressive style…Yes, Claude has outputted grammar, composition, and style that the underlying LLM distilled from thousands of works. But if someone were to read all the modern-day classics because of their exceptional expression, memorize them, and then emulate a blend of their best writing, would that violate the Copyright Act? Of course not.

“Like any reader aspiring to be a writer, Anthropic’s LLMs trained upon works not to race ahead and replicate or supplant them—but to turn a hard corner and create something different,” the ruling said.

Under this legal theory, all the company needed to do was buy every book it pirated to lawfully train its models, something that certainly costs less than $3,000 per book. But as the New York Times notes, this settlement won’t set any legal precedent that could determine future cases because it isn’t going to trial.

Get to know an artificial intelligence stock that other investors are just catching on to.

One stock that is not on the radar of most mainstream investors has quietly risen by more than 300% since April 2025, moving from an intraday low of $6.27 per share all the way to an intraday high of $26.43 per share in late August. Previously, the stock had peaked at over $50 per share in 2024. What changed? It became an artificial intelligence (AI) stock after suffering in the downturn of the electric vehicle market. Most investors probably haven’t caught on yet, and, until recently, the company may not have recognized the AI opportunity it had, either.

I’m referring to Aehr Test Systems (AEHR -2.81%), and I’ll explain why this company is crucial to the AI and data center industries. There is still a significant opportunity for investors to capitalize on, even if they missed the bottom.

Why is Aehr critical to AI?

Here is the 30,000-foot view. When companies, notably hyperscalers, build massive data centers full of tens of millions, and sometimes hundreds of millions, of semiconductors (chips), they must ensure that they are reliable. High failure rates are extremely costly in terms of remediation, labor, downtime, and replacements. If the company selling the chips has a high failure rate, its competitors can gain traction. Aehr Test Systems provides the necessary reliability testing systems.

Their importance cannot be understated. The latest chips are stackable (multiple layers of chips forming one unit), which allows for exponentially more processing power. However, there is a catch. Many times, they are a “single point of failure.” In other words, if one chip in the stack fails, the entire stack fails. The importance of reliability testing has increased by an order of magnitude as a result. And now Aehr is the hot name that could become a stock market darling again.

Image source: Getty Images.

Is Aehr stock a buy now?

You have probably heard about the massive data centers that the “hyperscalers,” companies like Meta Platforms, Amazon, Elon Musk’s xAI, and other tech giants, are building across the country and the world. In fact, trying to keep up with all of the announcements of new projects would make your head spin. In many cases, the data center campus spans more than a square mile and contains hundreds of thousands of chips. Elon Musk’s xAI project, dubbed “Colossus,” is said to require over a million GPUs in the end.

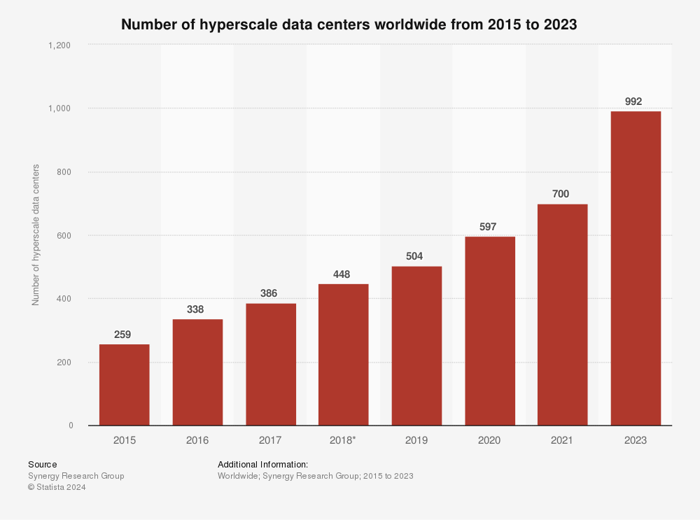

As shown below, the number of hyperscale data centers is soaring with no end in sight.

Source: Statista.

This number increased to more than 1,100 at the end of 2024, nearly doubling over the past five years. The demand is primarily driven by artificial intelligence, which is why Aehr is now an “AI stock” — and the reason its share price took off and could continue higher over the long term.

Aehr still faces serious challenges. Its revenue fell from $66 million in fiscal 2024 to $59 million in fiscal 2025. It slipped from an operating profit of $10 million to a loss of $6 million over that period as the company undertook the challenging task of refocusing its business. However, investors who dig deeper see a very encouraging sign. The company’s backlog (orders that have been placed, but not yet fulfilled) jumped to $15 million from $7 million. Aehr also announced several orders received from major hyperscalers over the last couple of months.

It’s challenging to value Aehr stock at this time. The company is in a transition period, and while the AI market looks hugely promising, it is still a work in progress. In its heyday, the stock’s valuation peaked at 31 times sales, and as recently as August 2023 it traded for 24 times sales compared to 12 times sales today. The AI market could be a gold mine for Aehr, and Aehr stock looks like a terrific buy for investors.

Bradley Guichard has positions in Aehr Test Systems and Amazon. The Motley Fool has positions in and recommends Amazon and Meta Platforms. The Motley Fool has a disclosure policy.

-

Business1 week ago

Business1 week agoThe Guardian view on Trump and the Fed: independence is no substitute for accountability | Editorial

-

Tools & Platforms4 weeks ago

Building Trust in Military AI Starts with Opening the Black Box – War on the Rocks

-

Ethics & Policy1 month ago

Ethics & Policy1 month agoSDAIA Supports Saudi Arabia’s Leadership in Shaping Global AI Ethics, Policy, and Research – وكالة الأنباء السعودية

-

Events & Conferences4 months ago

Events & Conferences4 months agoJourney to 1000 models: Scaling Instagram’s recommendation system

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoMumbai-based Perplexity Alternative Has 60k+ Users Without Funding

-

Education2 months ago

Education2 months agoVEX Robotics launches AI-powered classroom robotics system

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoHappy 4th of July! 🎆 Made with Veo 3 in Gemini

-

Funding & Business2 months ago

Funding & Business2 months agoKayak and Expedia race to build AI travel agents that turn social posts into itineraries

-

Education2 months ago

Education2 months agoMacron says UK and France have duty to tackle illegal migration ‘with humanity, solidarity and firmness’ – UK politics live | Politics

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoOpenAI 🤝 @teamganassi