AI Insights

1 Artificial Intelligence (AI) Stock Will Be Worth More Than Palantir Technologies and Amazon Combined by 2030

-

Palantir’s meteoric rise throughout the artificial intelligence (AI) revolution is impressive, but the stock remains historically — and potentially unsustainably — pricey.

-

Amazon has a number of well-positioned AI initiatives in the works, but scaling these ambitions will take many years.

-

Taiwan Semiconductor Manufacturing could be on the cusp of a major breakout fueled by ongoing AI infrastructure investment.

-

10 stocks we like better than Taiwan Semiconductor Manufacturing ›

Today, just 10 public companies command a market capitalization above $1 trillion. This elite trillion-dollar club includes Nvidia, Microsoft, Apple, Alphabet, Amazon (NASDAQ: AMZN), Meta Platforms, Broadcom, Taiwan Semiconductor Manufacturing (NYSE: TSM), Berkshire Hathaway, and Tesla.

Outside this cohort, several high-growth names are chasing the trillion-dollar milestone. Palantir Technologies (NASDAQ: PLTR), now among the largest technology stocks as measured by market cap, is one of them. Together with Amazon — an e-commerce and cloud computing giant aggressively layering artificial intelligence (AI) across its platforms — these two companies represent nearly $2.8 trillion in market value.

Both Palantir and Amazon are positioned to ride the AI wave for years to come. Yet, by 2030, I see Taiwan Semi emerging as more valuable than Palantir and Amazon combined.

I think Taiwan Semi remains largely overlooked among AI stocks, and the chip powerhouse could be the biggest winner over the remainder of the decade.

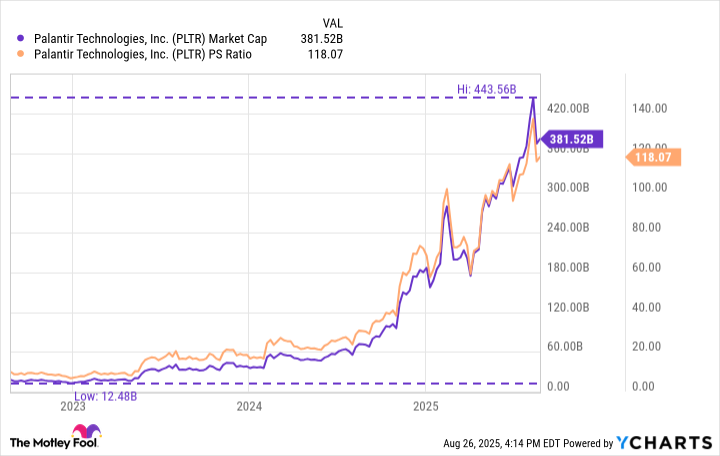

At the outset of the AI revolution, Palantir’s market cap stood at roughly $12 billion. Today, that figure ballooned to nearly $400 billion — placing the company ahead of enterprise software heavyweights such as SAP, Salesforce, and Adobe.

Indeed, Palantir has swiftly become a crucial operating system for large enterprises and government agencies around the world. That said, the pace of its valuation expansion is difficult to reconcile and should not be glossed over in favor of industry-specific metrics as opposed to tried-and-true valuation methodologies.

History shows that when stock prices run well beyond the underlying fundamentals of the business, corrections are often unavoidable.

The key risk with Palantir is that expectations will increasingly be measured against actual results and growth rates, rather than aspirational narratives or visionary rhetoric from management.

While I remain bullish on Palantir’s long-term runway, the stock appears historically overextended in the near term. A valuation reset is a possibility, which could leave the stock trading sideways for years if enthusiasm fades.

AI Insights

Prediction: This Monster Artificial Intelligence (AI) Chip Stock Will Soar in September (Hint: It’s Not Nvidia)

Broadcom is scheduled to report earnings on Sept. 4.

Over the past several weeks, investors have been bombarded with a wave of updates as companies reported earnings results for the second calendar quarter. For technology investors, artificial intelligence (AI) remains the dominant theme fueling the sector higher.

As I write this (mid-day on Aug. 27), all of the “Magnificent Seven” have posted earnings — with the lone exception being Nvidia (NVDA -3.38%), which reports later today. Still, the breadcrumbs left by big tech point to an undeniable trend: Spending on AI infrastructure is accelerating.

While this is undeniably bullish for graphics processing unit (GPU) leaders like Nvidia and Advanced Micro Devices, it also creates a powerful tailwind for systems integration specialist Broadcom (AVGO -3.70%).

With Broadcom slated to report earnings on Sept. 4, I predict the stock is well-positioned to rally.

Let’s explore why I’m optimistic about Broadcom’s upcoming earnings report, and assess whether the stock is a compelling buy at current levels.

Follow big tech’s breadcrumbs

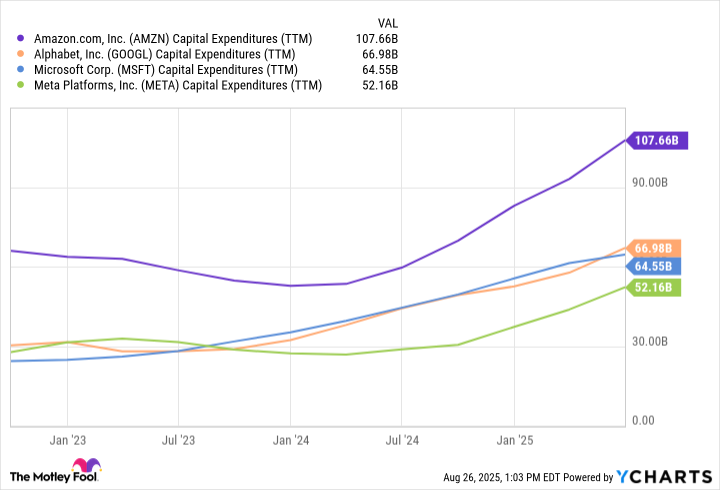

Global hyperscalers such as Amazon, Alphabet, Microsoft, and Meta Platforms have been spending record sums on capital expenditures (capex) over the last few years. While this clearly bodes well for Nvidia and AMD, Broadcom has also been a quiet beneficiary of rising AI infrastructure investment.

Data by YCharts.

One of Broadcom’s key AI growth drivers comes from its application-specific integrated circuits (ASICs) business. These custom silicon solutions allow customers to design chips that are optimized for their unique workloads.

By integrating purpose-built performance with compute power efficiency, Broadcom’s ASICs help hyperscalers lower their total cost of infrastructure relative to relying solely on off-the-shelf accelerators from the likes of Nvidia. This becomes highly desirable as training and inferencing workloads scale and become increasingly complex as more sophisticated AI use cases unfold.

Broadcom’s networking division is also positioned to benefit materially from the ongoing AI infrastructure cycle. As big tech continues to pour hundreds of billions of dollars annually into GPU deployment, Broadcom’s supporting infrastructure becomes an indispensable unsung hero.

The company’s portfolio of high-performance switches, interconnects, and optical components delivers low-latency, high-bandwidth connectivity to keep next-generation accelerators running at full speed. In essence, the company’s networking gear represents a foundational layer of AI data center construction — ensuring scalability and efficiency as workloads expand.

Image source: Getty Images.

Management likes the stock — shouldn’t you?

With a forward price-to-earnings (P/E) multiple of 45, Broadcom certainly isn’t trading at a discount. In fact, its multiple sits near peak levels seen during the AI revolution.

Data by YCharts.

Even so, the company’s board of directors authorized a $10 billion stock buyback program back in April. Share buybacks at elevated valuations can point to a strong signal: Management remains confident in Broadcom’s long-term growth trajectory, underscored by ongoing hyperscaler investment. On a more subtle note, sometimes companies repurchase their own shares when management thinks the stock is undervalued.

These dynamics could suggest that Broadcom is positioned for sustained, robust earnings growth, which could fuel further valuation expansion — even in the face of a premium multiple.

Is Broadcom stock a buy right now?

For the last few years, the AI trade has largely surrounded Nvidia and the cloud hyperscalers. Yet as infrastructure spending accelerates, the scope of the AI opportunity is broadening to other mission-critical enablers such as Broadcom. Custom chips, high-performance networking equipment, and integrated systems are now just as essential as securing GPUs — and Broadcom sits squarely at this intersection.

In my eyes, Broadcom is approaching its own “Nvidia moment” — a potential inflection where the narrative begins to recognize Broadcom as a supporting pillar of AI infrastructure and not simply an ancillary beneficiary of these tailwinds.

Against this backdrop, I predict that Broadcom’s September earnings report will reinforce its strategic importance in the AI landscape — fueling investor enthusiasm and a further rerating of the stock. For these reasons, I see Broadcom as a compelling opportunity to buy and hold over a long-term time horizon.

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

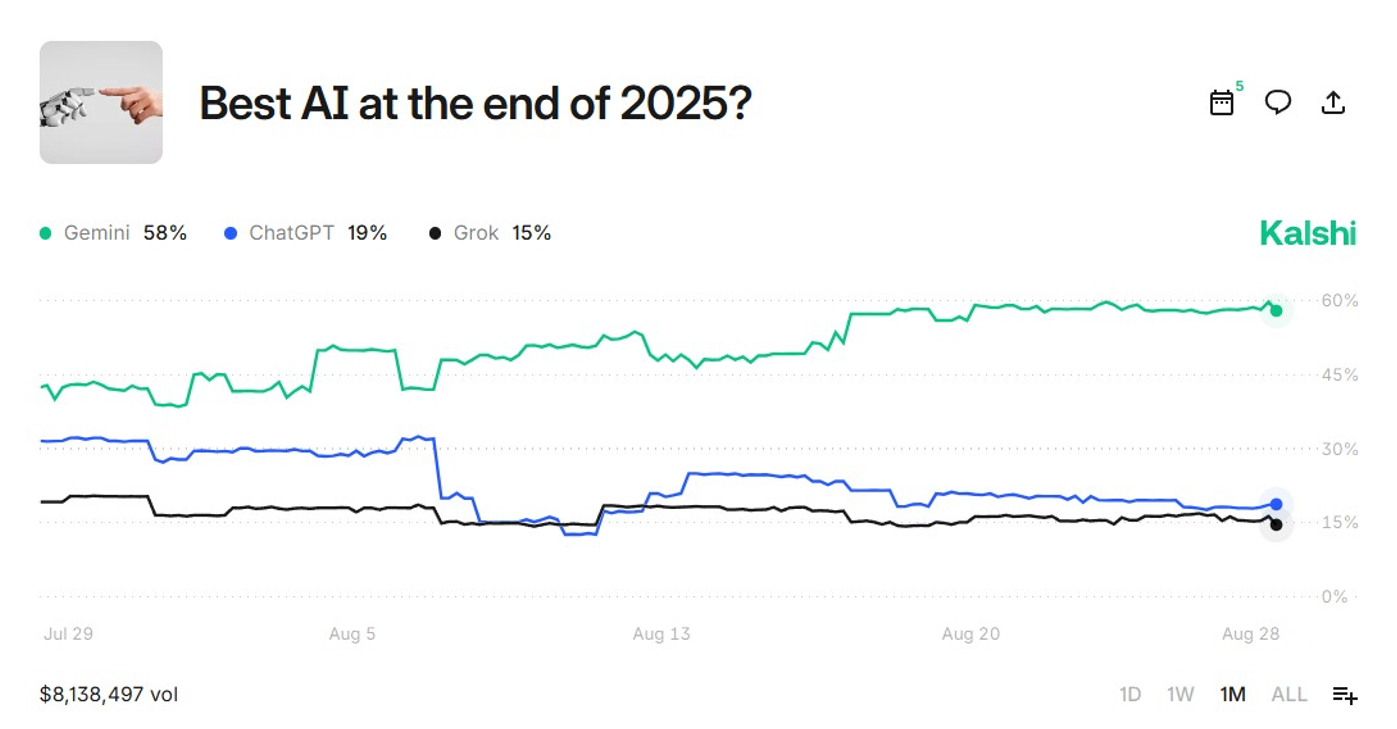

Sports gambling has DraftKings. Political junkies have PredictIt. And now the world’s nerdiest corner — the artificial intelligence (AI) scene — has its own set of bettors, where people wager actual money on whether Google’s Gemini will dunk on OpenAI’s GPT-5 this month.

TORONTO — As the rapid, unregulated development of artificial intelligence continues, the language people in Silicon Valley use to describe it is becoming increasingly religious.

From predicting the potential destruction of humanity to a transhumanist apocalypse where people merge with AI, here’s what some of the key players are saying.

___

“I think religion will be in trouble if we create other beings. Once we start creating beings that can think for themselves and do things for themselves, maybe even have bodies if they’re robots, we may start realizing we’re less special than we thought. And the idea that we’re very special and we were made in the image of God, that idea may go out the window.”

— Nobel Prize winner Geoffrey Hinton, often dubbed the “Godfather of AI” for his pioneering work on deep learning and neural networks.

___

“By 2045, which is only 20 years from now, we’ll be a million times more powerful. And we’ll be able to have expertise in every field.”

— author and computer scientist Ray Kurzweil, who believes humans will merge with AI.

___

“There certainly are dimensions of the technology that have become extremely powerful in the last century or two that have an apocalyptic dimension. And perhaps it’s strange not to try to relate it to the biblical tradition.”

— PayPal and Palantir co-founder Peter Thiel speaking to the Hoover Institution at Stanford University.

___

“I feel that the four big AI CEOs in the U.S. are modern-day prophets with four different versions of the Gospel and they’re all telling the same basic story that this is so dangerous and so scary that I have to do it and nobody else.”

— Max Tegmark, a physicist and machine learning researcher at the Massachusetts Institute of Technology.

___

“When people in the tech industry talk about building this one true AI, it’s almost as if they think they’re creating God or something.”

— Meta CEO Mark Zuckerberg on a podcast promoting his company’s own venture into AI.

___

“Everyone (including AI companies!) will need to do their part both to prevent risks and to fully realize the benefits. But it is a world worth fighting for. If all of this really does happen over 5 to 10 years — the defeat of most diseases, the growth in biological and cognitive freedom, the lifting of billions of people out of poverty to share in the new technologies, a renaissance of liberal democracy and human rights — I suspect everyone watching it will be surprised by the effect it has on them.”

— Anthropic CEO Dario Amodei in his essay, “Machines of Loving Grace: How AI Could Transform the World for the Better.”

___

“You and I are living through this once-in-human-history transition where humans go from being the smartest thing on planet Earth to not the smartest thing on planet Earth.”

— OpenAI CEO Sam Altman during an interview for TED Talks.

___

“These really big, scary problems that are complex and challenging to address — it’s so easy to gravitate towards fantastical thinking and wanting a one-size-fits-all global solution. I think it’s the reason that so many people turn to cults and all sorts of really out there beliefs when the future feels scary and uncertain. I think this is not different than that. They just have billions of dollars to actually enact their ideas.”

— Dylan Baker, lead research engineer at the Distributed AI Research Institute.

-

Tools & Platforms3 weeks ago

Building Trust in Military AI Starts with Opening the Black Box – War on the Rocks

-

Ethics & Policy1 month ago

Ethics & Policy1 month agoSDAIA Supports Saudi Arabia’s Leadership in Shaping Global AI Ethics, Policy, and Research – وكالة الأنباء السعودية

-

Events & Conferences3 months ago

Events & Conferences3 months agoJourney to 1000 models: Scaling Instagram’s recommendation system

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoMumbai-based Perplexity Alternative Has 60k+ Users Without Funding

-

Funding & Business2 months ago

Funding & Business2 months agoKayak and Expedia race to build AI travel agents that turn social posts into itineraries

-

Education2 months ago

Education2 months agoVEX Robotics launches AI-powered classroom robotics system

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoHappy 4th of July! 🎆 Made with Veo 3 in Gemini

-

Podcasts & Talks2 months ago

Podcasts & Talks2 months agoOpenAI 🤝 @teamganassi

-

Mergers & Acquisitions2 months ago

Mergers & Acquisitions2 months agoDonald Trump suggests US government review subsidies to Elon Musk’s companies

-

Jobs & Careers2 months ago

Jobs & Careers2 months agoAstrophel Aerospace Raises ₹6.84 Crore to Build Reusable Launch Vehicle